How to build a clear title workflow that actually prevents delays

Most closing delays are preventable. This is the workflow that stops them before they start.

Share article:

Michelle Artreche

5 minutes

Title Industry

Mar 25, 2026

Apr 22, 2026

You've done everything right. The closing is tomorrow, but now there’s a problem: someone found an old lien from 2016. This could delay the entire deal.

You're scrambling through emails and making callbacks with no documentation. The buyer's lender is asking for proof that you completed the due diligence, which you know you did, but you can’t show it.

Most closing delays are preventable. This is the workflow that stops them before they start. You'll walk away with a step-by-step process that catches defects early, keeps every party accountable, and gives you the documentation to prove it — before anyone asks.

What is a clear title and why does it matter in real estate?

A clear title is a property title free from liens, encumbrances, disputes, or competing ownership claims. That definition sounds straightforward, but failing to spot any issues can lead to serious problems.

Here's why it matters for everyone at the table:

- Buyers are protected from inheriting debt, unresolved legal disputes, or ownership claims they didn't know existed. If there’s no clear title, someone can challenge your ownership after closing.

- Sellers benefit from establishing credibility early, preventing last-minute deal collapses, and giving lenders what they need to work quickly.

- Lenders won't fund a mortgage without a confirmed, clear title. This is a must, no exceptions.

From a legal standpoint, title defects under U.S. real estate law can void transfers entirely. The specifics vary by state, so it’s important to check your local laws and consult a real estate attorney if you’re unsure.

What is a clear title workflow?

A clear title workflow is a series of repeatable steps that you follow to confirm that a property’s title is free of defects before closing. Viewing it as a workflow in real estate, rather than just an end result, is important. It turns a set of scattered tasks into a clear process with accountability at each stage.

The gap most teams face is this: title searches happen, but verification steps are often manual, fragmented, and undocumented. Files get marked as "fully processed" when critical verification steps are still missing. Those blind spots tend to surface at the worst possible time, days before closing, when there's no time to fix them.

Treating a clear title as a workflow is what separates closings that run smoothly from ones that collapse at the finish line.

Who is involved in the clear title process?

Understanding who owns each step prevents miscommunication and delays. Key parties include:

- Buyer and seller (or their attorneys): Initiate the transaction and provide necessary documentation

- Title company or title agent: Conducts the search, manages curative work, and issues the commitment

- Real estate attorneys: Review title exceptions and resolve complex defects that require legal intervention

- Lender: Requires a clear title and title insurance before funding is released

- County recorder's office: The source of public records for deeds, liens, and encumbrances

Each party relies on the others. If one step is delayed without clear information, say, a file sitting between a processor and a closer without a defined handoff, it can disrupt the whole process. As a title professional, your job is to complete your steps and make sure transitions between parties are defined, documented, and followed every time.

The clear title workflow: Step by step

Every step below should be documented, time-stamped, and traceable. If it's being handled through informal phone calls or unlogged emails, you have a gap in your workflow.

Step 1: Open a title order

The title order is typically initiated by the buyer's agent, lender, or escrow officer. It includes the property address, legal description, and transaction details.

Starting early gives the rest of the workflow room to breathe. If you wait until two weeks before closing to order the title, you've already lost the buffer you need if defects surface. Open the order the moment a contract is executed.

Step 2: Conduct the title search

During the title search, you examine public records — deeds, mortgages, court judgments, tax records, and property indexes. Search depth typically goes back 40–60 years, depending on state requirements and underwriter guidelines.

State-specific nuances matter here, and this is where local knowledge pays off:

- Texas: Title searches must account for homestead protections under the Texas Property Code (Tex. Prop. Code §41.001), which can affect how liens attach to the property.

- New York: Searches routinely include surrogate court records for inherited properties, particularly in areas with older housing stock where estate transfers are common.

- Florida: Given high levels of foreign investment in real estate, searchers often verify compliance with FIRPTA withholding requirements (26 U.S.C. §1445) during the title review process.

If you're working across state lines, don't guess. Partner with someone who knows the local requirements cold.

Step 3: Review the title commitment or abstract

The title commitment outlines conditions that must be met before the policy is issued. Key items include legal description accuracy, current vesting, and Schedule B exceptions — easements, restrictions, and existing liens.

This is where most defects first become visible. Review it carefully, and don't treat it as a formality.

One common example: a seller's attorney may attempt to block closing charges to the seller despite contract language that clearly states otherwise.

The issue often stems from the fact that no one flagged the conflict early enough to resolve it before the closing date. A thorough commitment review would have caught it weeks earlier. That's time you can't get back.

Step 4: Identify title defects

Common defects that delay or derail closings include:

- Unpaid liens (tax, mechanic's, judgment)

- Boundary or survey disputes

- Recording errors in public records

- Unknown heirs or forged documents

- Unreleased mortgages or satisfactions never recorded

- Easements or encroachments not disclosed

Some of these are straightforward to fix. Others require legal intervention and can take months. The sooner you identify them, the more options you have — and the less pressure everyone is under to make rushed decisions.

Step 5: Resolve title defects (curative work)

Every defect has a resolution path: lien payoffs, affidavits, quiet title actions, and corrective deeds. Timelines vary significantly. A missing satisfaction may take days. A quiet title action can take months. Attorneys handle the complex legal issues; escrow teams track status and deadlines.

This is where undocumented workflows do the most damage. If there's no record of what was resolved and by whom, liability exposure increases for everyone involved.

Consider this scenario: a lender's documents arrive the day of closing, balanced, and scheduled — all within hours.

The deal closes, but only because the team had a documented process for emergency balancing. Without that structure, the closing would have been rescheduled, and all parties would have spent their time pointing fingers instead of solving the problem.

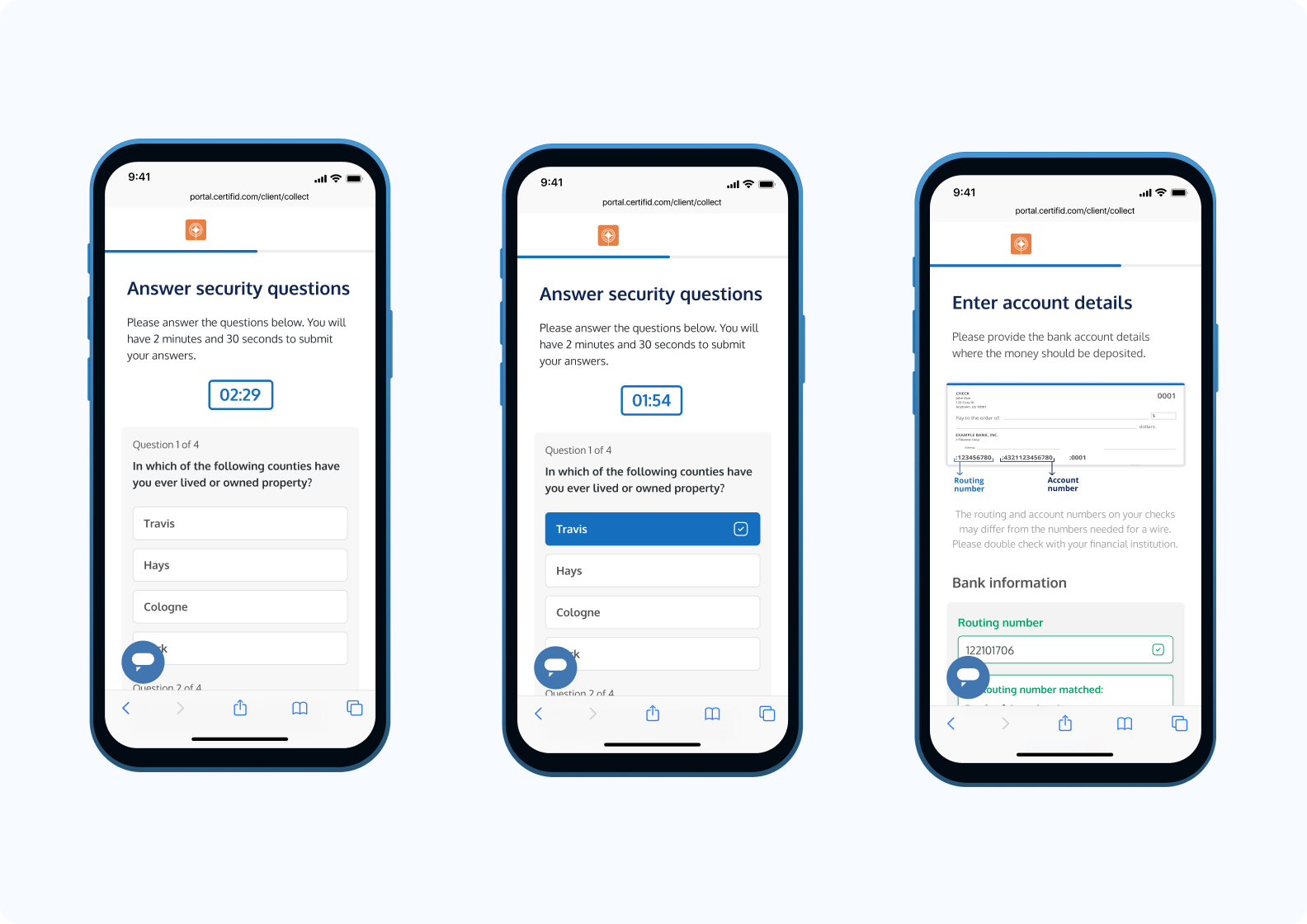

Step 6: Verify parties and wire instructions

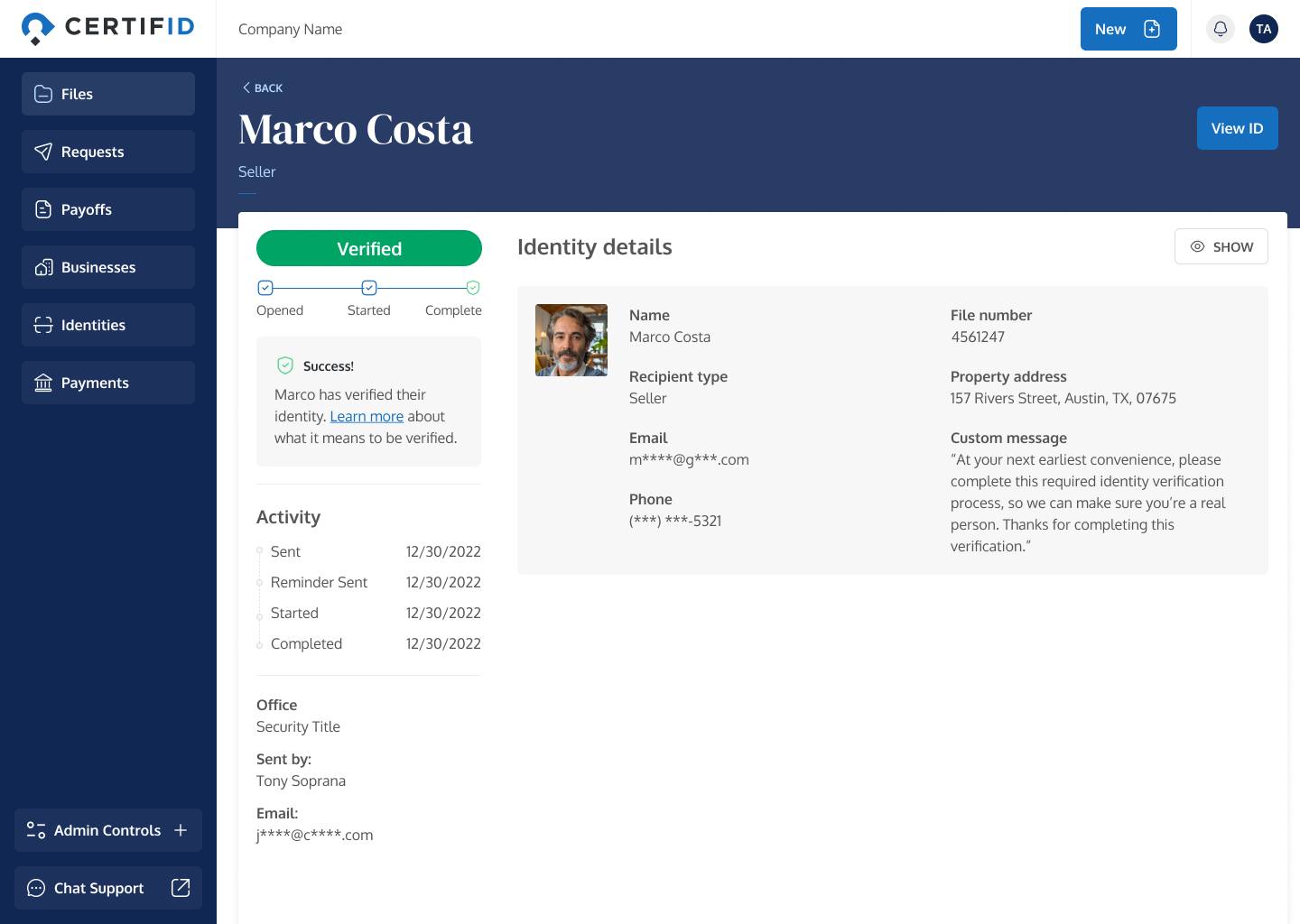

This is where fraud risk is highest, and where most manual workflows break down. Two things need to happen before any money moves: verify who you're dealing with, and verify where the money is going.

Verify identities with CertifID Match

This step is especially critical for sellers in vacant land or out-of-state transactions — the most common impersonation targets.

Match scans government-issued IDs against 250+ global databases, confirms liveness through biometric selfie detection (catching deepfakes and photos of photos), and evaluates 150+ fraud indicators, including device verification and geolocation.

No app download, no portal, no SSN required.

Secure wire instructions through CertifID

Whether you're sharing your wiring instructions with a buyer or collecting banking details from a seller, CertifID replaces the email-and-PDF approach that puts instructions in the exact channel fraudsters compromise. Parties receive a secure, branded link — details are verified, confirmed, and backed by insurance.

Both products produce documented, auditable records. Pushback like "we already verified this" is exactly why verification must be centralized and traceable.

Step 7: Issue title insurance

There are two policies to understand:

- Owner's policy: Protects the buyer. Optional but strongly recommended.

- Lender's policy: Protects the lender. Typically required for mortgage approval.

Title insurance covers losses from defects not discovered during the search. It's the safety net for the entire workflow. Without it, buyers and lenders absorb the full financial risk of hidden defects that surface after closing.

Step 8: Close and record

Clear title confirmed. Closing documents executed. Funds disbursed. The deed and mortgage are recorded with the county recorder's office.

The workflow is complete only when recording is confirmed — not when signatures are collected. Recording is what confirms the public record reflects the transaction. Until that happens, the title isn't truly clear.

Every step above should produce a documented artifact. If it doesn't, the workflow has a gap.

How long does the clear title workflow take?

Timelines depend on the property, the jurisdiction, and whether defects are found. Realistic expectations:

- Clean title, no defects: Typically 1–2 weeks from title order to commitment

- Minor defects (unreleased lien, recording error): Add 1–2 weeks for curative work

- Major defects (boundary dispute, unknown heir, quiet title action): Can extend weeks to months

Common factors that slow things down: unresponsive lenders, missing documentation, and manual verification processes with no tracking.

In one real scenario, a seller's attorney refused to prepare seller documents or allow closing fees, citing contract interpretation disputes. The delay was about the absence of a documented escalation process to resolve disagreements before the closing date arrived.

Starting the title order early in the transaction is the single most effective way to protect the closing date.

Tips to streamline your clear title workflow

Efficiency means eliminating the manual steps that create risk without adding value — not cutting corners. Here's how to tighten up the process:

- Order the title search the moment a contract is executed. Don't wait for financing approval. This one sounds obvious until you're two days from closing and realize no one did it.

- Use a closing checklist that tracks each workflow step with timestamps and responsible parties. If it's not on the checklist, it doesn't exist.

- Address known title issues early. Sellers should do this before listing; agents before contract ratification. Surprises at closing are almost always problems that were visible earlier.

- Replace manual phone-based verification with documented, auditable identity and wire verification processes. The phone call you made isn't proof. The verified record is.

- Keep all parties updated on defect resolution status in a centralized system — not scattered emails.

State-specific example: In California, where community property rules apply (Cal. Fam. Code §760), confirming spousal interest early prevents last-minute title objections.

Many experienced professionals won't even schedule loan closings until they have clear-to-close confirmation from the lender — because rescheduling frustrated clients is a bigger problem than asking someone to wait a few extra days.

The best workflows leave a clear trail at every step.

Common challenges in the clear title workflow and how to address them

These breakdowns happen more often than they should. Here's how to recognize them before they derail a closing.

Last-minute defects surfacing

Defects identified days before closing leave no time to resolve them. The root cause is almost always starting the title search too late or treating the commitment review as a formality. The fix: order title early and treat the commitment as an active document throughout the transaction.

Lack of documentation on curative work

Without documentation, no one can prove who was responsible for resolving a lien or recording a satisfaction.

When something goes wrong, liability questions go unanswered, and finger-pointing begins. The solution is to create a single shared space where every action is recorded — including who did it, when it happened, and what the result was. Make this a must for your entire team.

Wire fraud and identity verification gaps

Some professionals refuse to close without completing identity verification, even when other parties claim they've already done it. That instinct is correct.

"We already verified this" is not a documented record. The fix: use a secure digital verification platform like CertifID and document every verification step. Never rely on email-based confirmations for wire instructions.

These challenges are predictable. The workflow exists to prevent them, but only if it's actually followed.

Clear title workflow: Improve operations within your company

Title professionals who close clean, every time, aren't luckier than everyone else. They built a better process. Here’s how to build your own.

To have a clear title workflow, you need to build, document, and repeat. Every lien checked, every identity verified, every wire instruction confirmed through a secure channel protects your closing, your clients, and your reputation.

Whether you're processing five files a week or fifty, the workflow should be the same: structured, traceable, and designed to surface problems before they become crises. If your current process has steps that exist only in someone's memory, that's the first gap to close.

The second is identity verification. CertifID Match verifies transaction participants quickly, scanning IDs against over 250 global databases, confirming real-life presence with biometric checks, and analyzing more than 150 fraud indicators.

There are no app downloads, no portals, and no Social Security numbers needed. Every verification is backed by insurance.

FAQ

How far back does a title search go?

Typically 40–60 years, depending on state requirements and underwriter guidelines. Some states require a full search back to sovereignty, while others allow limited searches if prior title insurance policies exist.

Our closer says they need fully processed files two weeks before closing. Is that realistic?

It depends on volume. Some closers handling 75+ files a month need a full week to review and balance. Others say two business days is enough. The real issue is the handoff — when files sit between the processor and closer with no clear protocol, things fall through. A shared checklist with timestamps keeps everyone accountable.

What if another firm on the transaction refuses to complete identity verification?

This happens more than it should. Pushback like "we already verified this" is exactly why verification needs to be documented and centralized — not assumed. If you can't confirm who's on the other side of the transaction, don't close.

Is there a standard SOP for handing off files from processor to closer?

No universal standard, but effective teams use a shared email and a file checklist tracking what's ordered, received, and outstanding. The file should move to the closer once everything is ordered — not once everything is back. Pending items are fine as long as they're documented.

What's the biggest risk in a clear title workflow that teams overlook?

Undocumented steps. Searches happen, curative work gets done, wires get confirmed — but without timestamps and responsible parties logged, there's no audit trail. When something goes wrong, no one can prove what was done or by whom.

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

You've done everything right. The closing is tomorrow, but now there’s a problem: someone found an old lien from 2016. This could delay the entire deal.

You're scrambling through emails and making callbacks with no documentation. The buyer's lender is asking for proof that you completed the due diligence, which you know you did, but you can’t show it.

Most closing delays are preventable. This is the workflow that stops them before they start. You'll walk away with a step-by-step process that catches defects early, keeps every party accountable, and gives you the documentation to prove it — before anyone asks.

What is a clear title and why does it matter in real estate?

A clear title is a property title free from liens, encumbrances, disputes, or competing ownership claims. That definition sounds straightforward, but failing to spot any issues can lead to serious problems.

Here's why it matters for everyone at the table:

- Buyers are protected from inheriting debt, unresolved legal disputes, or ownership claims they didn't know existed. If there’s no clear title, someone can challenge your ownership after closing.

- Sellers benefit from establishing credibility early, preventing last-minute deal collapses, and giving lenders what they need to work quickly.

- Lenders won't fund a mortgage without a confirmed, clear title. This is a must, no exceptions.

From a legal standpoint, title defects under U.S. real estate law can void transfers entirely. The specifics vary by state, so it’s important to check your local laws and consult a real estate attorney if you’re unsure.

What is a clear title workflow?

A clear title workflow is a series of repeatable steps that you follow to confirm that a property’s title is free of defects before closing. Viewing it as a workflow in real estate, rather than just an end result, is important. It turns a set of scattered tasks into a clear process with accountability at each stage.

The gap most teams face is this: title searches happen, but verification steps are often manual, fragmented, and undocumented. Files get marked as "fully processed" when critical verification steps are still missing. Those blind spots tend to surface at the worst possible time, days before closing, when there's no time to fix them.

Treating a clear title as a workflow is what separates closings that run smoothly from ones that collapse at the finish line.

Who is involved in the clear title process?

Understanding who owns each step prevents miscommunication and delays. Key parties include:

- Buyer and seller (or their attorneys): Initiate the transaction and provide necessary documentation

- Title company or title agent: Conducts the search, manages curative work, and issues the commitment

- Real estate attorneys: Review title exceptions and resolve complex defects that require legal intervention

- Lender: Requires a clear title and title insurance before funding is released

- County recorder's office: The source of public records for deeds, liens, and encumbrances

Each party relies on the others. If one step is delayed without clear information, say, a file sitting between a processor and a closer without a defined handoff, it can disrupt the whole process. As a title professional, your job is to complete your steps and make sure transitions between parties are defined, documented, and followed every time.

The clear title workflow: Step by step

Every step below should be documented, time-stamped, and traceable. If it's being handled through informal phone calls or unlogged emails, you have a gap in your workflow.

Step 1: Open a title order

The title order is typically initiated by the buyer's agent, lender, or escrow officer. It includes the property address, legal description, and transaction details.

Starting early gives the rest of the workflow room to breathe. If you wait until two weeks before closing to order the title, you've already lost the buffer you need if defects surface. Open the order the moment a contract is executed.

Step 2: Conduct the title search

During the title search, you examine public records — deeds, mortgages, court judgments, tax records, and property indexes. Search depth typically goes back 40–60 years, depending on state requirements and underwriter guidelines.

State-specific nuances matter here, and this is where local knowledge pays off:

- Texas: Title searches must account for homestead protections under the Texas Property Code (Tex. Prop. Code §41.001), which can affect how liens attach to the property.

- New York: Searches routinely include surrogate court records for inherited properties, particularly in areas with older housing stock where estate transfers are common.

- Florida: Given high levels of foreign investment in real estate, searchers often verify compliance with FIRPTA withholding requirements (26 U.S.C. §1445) during the title review process.

If you're working across state lines, don't guess. Partner with someone who knows the local requirements cold.

Step 3: Review the title commitment or abstract

The title commitment outlines conditions that must be met before the policy is issued. Key items include legal description accuracy, current vesting, and Schedule B exceptions — easements, restrictions, and existing liens.

This is where most defects first become visible. Review it carefully, and don't treat it as a formality.

One common example: a seller's attorney may attempt to block closing charges to the seller despite contract language that clearly states otherwise.

The issue often stems from the fact that no one flagged the conflict early enough to resolve it before the closing date. A thorough commitment review would have caught it weeks earlier. That's time you can't get back.

Step 4: Identify title defects

Common defects that delay or derail closings include:

- Unpaid liens (tax, mechanic's, judgment)

- Boundary or survey disputes

- Recording errors in public records

- Unknown heirs or forged documents

- Unreleased mortgages or satisfactions never recorded

- Easements or encroachments not disclosed

Some of these are straightforward to fix. Others require legal intervention and can take months. The sooner you identify them, the more options you have — and the less pressure everyone is under to make rushed decisions.

Step 5: Resolve title defects (curative work)

Every defect has a resolution path: lien payoffs, affidavits, quiet title actions, and corrective deeds. Timelines vary significantly. A missing satisfaction may take days. A quiet title action can take months. Attorneys handle the complex legal issues; escrow teams track status and deadlines.

This is where undocumented workflows do the most damage. If there's no record of what was resolved and by whom, liability exposure increases for everyone involved.

Consider this scenario: a lender's documents arrive the day of closing, balanced, and scheduled — all within hours.

The deal closes, but only because the team had a documented process for emergency balancing. Without that structure, the closing would have been rescheduled, and all parties would have spent their time pointing fingers instead of solving the problem.

Step 6: Verify parties and wire instructions

This is where fraud risk is highest, and where most manual workflows break down. Two things need to happen before any money moves: verify who you're dealing with, and verify where the money is going.

Verify identities with CertifID Match

This step is especially critical for sellers in vacant land or out-of-state transactions — the most common impersonation targets.

Match scans government-issued IDs against 250+ global databases, confirms liveness through biometric selfie detection (catching deepfakes and photos of photos), and evaluates 150+ fraud indicators, including device verification and geolocation.

No app download, no portal, no SSN required.

Secure wire instructions through CertifID

Whether you're sharing your wiring instructions with a buyer or collecting banking details from a seller, CertifID replaces the email-and-PDF approach that puts instructions in the exact channel fraudsters compromise. Parties receive a secure, branded link — details are verified, confirmed, and backed by insurance.

Both products produce documented, auditable records. Pushback like "we already verified this" is exactly why verification must be centralized and traceable.

Step 7: Issue title insurance

There are two policies to understand:

- Owner's policy: Protects the buyer. Optional but strongly recommended.

- Lender's policy: Protects the lender. Typically required for mortgage approval.

Title insurance covers losses from defects not discovered during the search. It's the safety net for the entire workflow. Without it, buyers and lenders absorb the full financial risk of hidden defects that surface after closing.

Step 8: Close and record

Clear title confirmed. Closing documents executed. Funds disbursed. The deed and mortgage are recorded with the county recorder's office.

The workflow is complete only when recording is confirmed — not when signatures are collected. Recording is what confirms the public record reflects the transaction. Until that happens, the title isn't truly clear.

Every step above should produce a documented artifact. If it doesn't, the workflow has a gap.

How long does the clear title workflow take?

Timelines depend on the property, the jurisdiction, and whether defects are found. Realistic expectations:

- Clean title, no defects: Typically 1–2 weeks from title order to commitment

- Minor defects (unreleased lien, recording error): Add 1–2 weeks for curative work

- Major defects (boundary dispute, unknown heir, quiet title action): Can extend weeks to months

Common factors that slow things down: unresponsive lenders, missing documentation, and manual verification processes with no tracking.

In one real scenario, a seller's attorney refused to prepare seller documents or allow closing fees, citing contract interpretation disputes. The delay was about the absence of a documented escalation process to resolve disagreements before the closing date arrived.

Starting the title order early in the transaction is the single most effective way to protect the closing date.

Tips to streamline your clear title workflow

Efficiency means eliminating the manual steps that create risk without adding value — not cutting corners. Here's how to tighten up the process:

- Order the title search the moment a contract is executed. Don't wait for financing approval. This one sounds obvious until you're two days from closing and realize no one did it.

- Use a closing checklist that tracks each workflow step with timestamps and responsible parties. If it's not on the checklist, it doesn't exist.

- Address known title issues early. Sellers should do this before listing; agents before contract ratification. Surprises at closing are almost always problems that were visible earlier.

- Replace manual phone-based verification with documented, auditable identity and wire verification processes. The phone call you made isn't proof. The verified record is.

- Keep all parties updated on defect resolution status in a centralized system — not scattered emails.

State-specific example: In California, where community property rules apply (Cal. Fam. Code §760), confirming spousal interest early prevents last-minute title objections.

Many experienced professionals won't even schedule loan closings until they have clear-to-close confirmation from the lender — because rescheduling frustrated clients is a bigger problem than asking someone to wait a few extra days.

The best workflows leave a clear trail at every step.

Common challenges in the clear title workflow and how to address them

These breakdowns happen more often than they should. Here's how to recognize them before they derail a closing.

Last-minute defects surfacing

Defects identified days before closing leave no time to resolve them. The root cause is almost always starting the title search too late or treating the commitment review as a formality. The fix: order title early and treat the commitment as an active document throughout the transaction.

Lack of documentation on curative work

Without documentation, no one can prove who was responsible for resolving a lien or recording a satisfaction.

When something goes wrong, liability questions go unanswered, and finger-pointing begins. The solution is to create a single shared space where every action is recorded — including who did it, when it happened, and what the result was. Make this a must for your entire team.

Wire fraud and identity verification gaps

Some professionals refuse to close without completing identity verification, even when other parties claim they've already done it. That instinct is correct.

"We already verified this" is not a documented record. The fix: use a secure digital verification platform like CertifID and document every verification step. Never rely on email-based confirmations for wire instructions.

These challenges are predictable. The workflow exists to prevent them, but only if it's actually followed.

Clear title workflow: Improve operations within your company

Title professionals who close clean, every time, aren't luckier than everyone else. They built a better process. Here’s how to build your own.

To have a clear title workflow, you need to build, document, and repeat. Every lien checked, every identity verified, every wire instruction confirmed through a secure channel protects your closing, your clients, and your reputation.

Whether you're processing five files a week or fifty, the workflow should be the same: structured, traceable, and designed to surface problems before they become crises. If your current process has steps that exist only in someone's memory, that's the first gap to close.

The second is identity verification. CertifID Match verifies transaction participants quickly, scanning IDs against over 250 global databases, confirming real-life presence with biometric checks, and analyzing more than 150 fraud indicators.

There are no app downloads, no portals, and no Social Security numbers needed. Every verification is backed by insurance.

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503