Safe earnest money transfers for title companies

Say goodbye to outdated payment processes. CertifID makes earnest money deposits fast, easy, and secure—with no checks, no wires, and no trips to the bank.

Share article:

Cheryl Crouse

10 minutes

Earnest Money Deposit

Aug 5, 2025

Apr 30, 2026

Safe earnest money transfers for title companies

Cybercrime losses reported to the FBI Internet Crime Complaint Center (IC3) have grown every year, reaching $16.6 billion in 2024.

Imagine a realistic threat: A fraudster intercepts an earnest money check from an overnight drop box using a washer attached to a fishing line. They then use AI-powered check washing techniques to alter the payee and amount. The earnest money deposit (EMD) gets redirected to the criminals' account, appearing completely legitimate.

Check fraud has increased nearly 400% since 2023. Traditional earnest money transfer methods now expose title companies to fraud and compliance risks daily, with similar attacks targeting real estate professionals across the country.

This guide explains how to implement secure, compliant earnest money transfers that protect your clients, your escrow accounts, and your reputation without slowing down your closing process.

What is earnest money?

Earnest money is a good-faith deposit that demonstrates a buyer's serious intent to purchase a property. It's typically held in escrow by a title company.

This deposit creates legal obligations for both parties and shows the seller that the buyer has the financial capacity to complete the transaction.

Earnest money typically ranges from 1-10% of the purchase price, varying by local market conditions and property value.

In competitive markets, buyers often offer higher earnest money deposits to strengthen their offers. The funds are typically due within 24-72 hours of contract acceptance, creating time pressure that fraudsters exploit.

Title companies have a legal obligation to safeguard these funds in securely maintained escrow accounts. Failing to do so can result in regulatory violations, underwriting issues, and professional liability exposure.

Earnest money by state: why good funds matter

Earnest money handling requirements vary by state. Some states enforce strict good funds laws, while others rely more heavily on fiduciary standards and professional judgment. While what’s compliant in one state may violate regulations in another, modern payment platforms have evolved to make it possible to deliver earnest money digitally without sacrificing good funds compliance or exposing escrow to reversals.

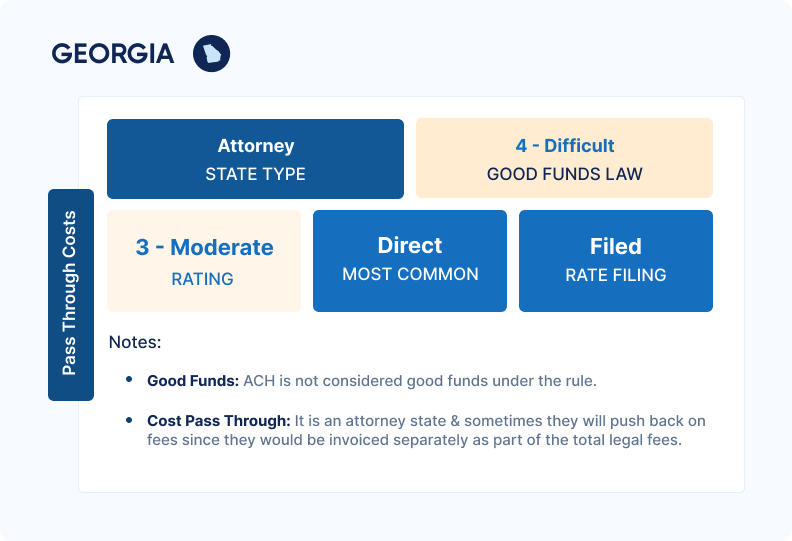

Georgia requires strict compliance with good funds laws, meaning ACH transfers are not acceptable for earnest money deposits. Title professionals must verify that deposits meet the state's certified funds requirements through wire transfers or cashier's checks.

Alabama offers more discretion, as it does not have a formal good funds statute. Title professionals are expected to rely on fiduciary duty and professional standards to determine acceptable payment methods.

For title companies operating across jurisdictions, compliance can get complicated. A secure digital payment platform with configurable workflows helps simplify the process. It reduces manual oversight and supports consistent adherence to local regulations.

Why security matters

Most earnest money transfer methods are irreversible once completed, making fraud prevention more critical than recovery. Unlike credit card chargebacks, wire transfers and certified funds can't be "undone" once fraudsters receive them. This makes your verification procedures the last line of defense against financial loss.

Major risks and vulnerabilities in earnest money transfers

Wire fraud schemes

Business Email Compromise (BEC): Criminals infiltrate email accounts to intercept and modify legitimate wire instructions, often making subtle changes to routing numbers or account details.

These attacks are sophisticated and can compromise even tech-savvy professionals who think they're following secure procedures.

EMD cancellation scams: Fraudsters send large deposits via cheque (often for amounts exceeding typical EMD, like $175,000 for a $150,000 property), then quickly cancel the transaction, citing contingencies like failed inspections or zoning issues.

They request wire refunds before the original check clears, leaving title companies liable when the check bounces. This scheme specifically targets vacant land transactions and involves impersonating both listing and buying agents to appear legitimate.

Traditional method weaknesses

Each traditional payment method creates specific vulnerabilities that fraudsters exploit.

Personal checks

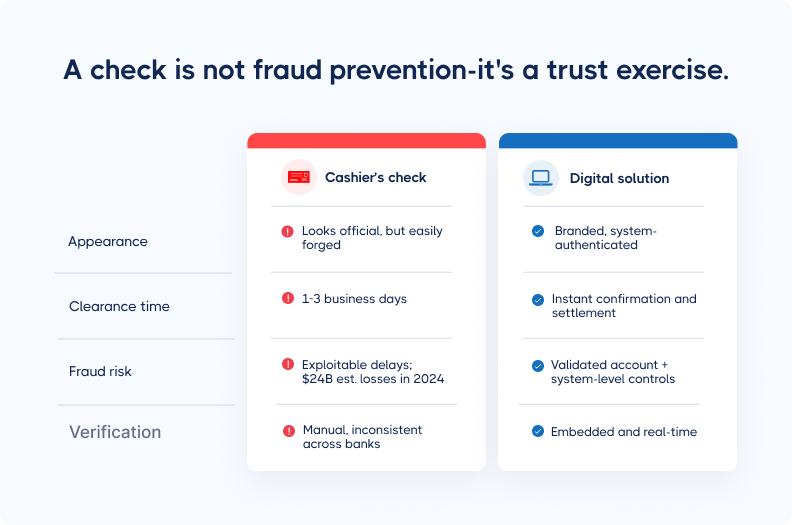

Check fraud is on the rise, with fraudsters using AI-powered techniques to create convincing forgeries.

Even certified checks can be fraudulent—fraudsters can intercept checks from overnight drop boxes using simple tools like washers on fishing line, then alter them using advanced check washing methods.

Our founder, Tom, experienced this firsthand in 2015.

His title company received a certified check for $180,000 that looked completely legitimate: genuine watermarks, security features, everything. Their business banker assured them it had cleared. They wired the refunds as requested, but the check was actually fraudulent and bounced days later after the wire was already sent.

The problem? Even certified checks can be sophisticated forgeries, and there's no consistent federal standard for verification across clearing houses. The clearing time window, where checks appear cleared but haven’t fully processed, creates a dangerous gap that fraudsters exploit. A secure, verified digital transfer eliminates this uncertainty.

For a detailed discussion of these check fraud tactics and how they've evolved with AI technology, watch our recent webinar "To Catch a Fraudster: Digital vs. Check Payments" where Tom and our payments expert Jason Campbell break down real-world fraud scenarios.

Wire transfers

Traditional wire transfers rely on emailed instructions that are easily spoofed or intercepted. Once sent, wires are nearly impossible to recover if they go to the wrong account.

Digital payment workflows can replace emailed instructions with secure, authenticated requests, eliminating this point of vulnerability and providing instant confirmation for all parties.

ACH transfers

ACH transfers can be reversed for up to 60 days in some cases, making them problematic for earnest money in states with good funds laws. Many states don't recognize ACH transfers as acceptable EMD deposits, creating compliance violations that can result in regulatory action.

That said, not all ACH transfers are created equal; modern digital payment platforms address these risks by verifying buyer identity, validating bank account ownership, and performing balance checks before funds are debited.

These layered controls reduce fraud, prevent unauthorized debits, and ensure payments are only initiated from verified accounts. Combined with controlled delivery and risk management, these platforms may offer compliant alternatives to traditional ACH.

Email vulnerabilities

Unencrypted email communications and account takeovers make traditional communication methods inherently unsafe for financial instructions.

Without centralized visibility of incoming payments, title companies often struggle to reconcile transactions. Modern platforms centralize payment data in one place, reducing manual matching errors and ensuring funds are quickly tied to the correct file.

Secure earnest money handling: 3 best practices

Protecting earnest money requires layered security that addresses both technical vulnerabilities and human error factors.

1. Identity verification protocols

Multi-factor authentication: Verify buyer identity through multiple independent channels—not just relying on email communications or phone calls. Fraudsters often compromise multiple communication methods simultaneously, so single-point verification creates dangerous vulnerabilities.

Document verification: Validate driver's licenses and other identification documents, checking for signs of forgery or alteration. Sophisticated fraudsters can create convincing fake IDs that pass visual inspection, so automated verification systems provide better detection rates.

Red flag identification: Watch for suspicious transaction indicators like rushed timelines, unusual payment methods, out-of-state parties with local properties, or buyers who resist verification procedures.

2. Written procedures and staff training

Standardized workflows: Document step-by-step verification processes that all staff must follow consistently. Ad-hoc procedures create vulnerabilities that fraudsters exploit, especially during busy periods when teams take shortcuts.

Annual training requirements: Provide regular staff education about evolving fraud tactics and new security threats. Fraudsters constantly adapt their methods, so training must keep pace with emerging schemes.

Escalation procedures: Define when staff should flag suspicious transactions and involve supervisors or security specialists in verification decisions. Junior staff shouldn't make security decisions alone, especially for high-value or unusual transactions.

Documentation standards: Maintain a clear audit trail that demonstrates verification procedures are strictly followed—for compliance and in the event of fraud investigations.

3. Technology security measures

Encrypted communications limitations: Even secure email isn't enough protection because BEC attacks take over entire email accounts, allowing fraudsters to send and receive emails that appear completely legitimate.

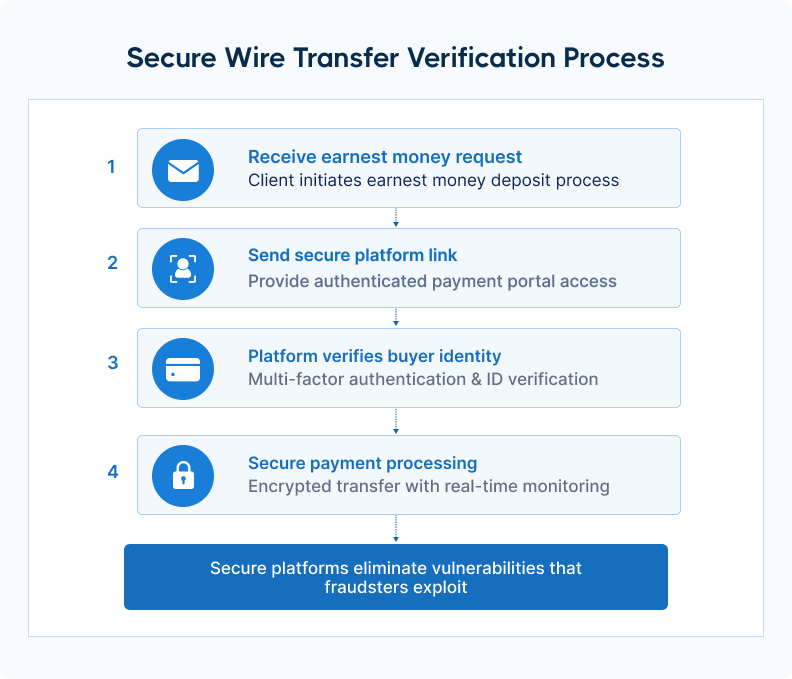

Secure payment platforms: Modern solutions like CertifID eliminate email-based wire instructions by providing secure, authenticated payment links that create trust from the outset.

Processing earnest money deposits within the same portal as other CertifID services ensures secure oversight and builds in fraud protection from day one.

Secure payment platforms remove the human error factor from instruction handling and provide tamper-proof payment processes. Compared to old-school methods, digital solutions guarantee safer transactions.

Real-time monitoring: Transaction tracking and alert systems provide immediate notification of unusual activity or failed verification attempts.

Digital payment solutions for earnest money transfers: Implementation guide

The risks and limitations of traditional payment methods highlight why secure digital platforms are becoming the new standard. Here's how they compare:

Transitioning from traditional payment methods to secure digital platforms is easier than many title companies expect, and it’s quickly becoming the industry standard for compliance and client experience.

Here’s a breakdown of the key phases involved in implementing a digital earnest money transfer solution.

Phase 1: Assessment and planning

Audit your current workflow: Start by mapping how earnest money deposits are currently collected. Identify friction points, gaps in documentation, and any exposure to manual errors or impersonation fraud.

Quantify the risk: Assess the number and average value of monthly EMD transactions. How much time does your team spend managing reconciliation for bounced checks and chasing down wire payments? This creates a baseline for improvement and a case for stakeholders.

Evaluate modern options: Look for platforms that reduce liability and manual overhead while improving the client experience. CertifID offers onboarding, SOC 2-compliant infrastructure, and direct insurance up to $5 million per file.

Budget with intention: Weigh fraud prevention and workflow efficiency against the potential cost of a single lost deposit. CertifID keeps onboarding light, requiring no extra tools or IT investment.

Secure buy-in: Present the shift as a competitive advantage. Emphasize protection, speed, and simplicity—not just for your team, but for agents and clients, too.

Phase 2: Platform selection and setup

Vendor evaluation criteria: Prioritize solutions with strong security credentials and real-time tracking.

Security validation: Verify encryption standards, identity verification protocols, and other security features that protect against fraud and ensure compliance with relevant regulations.

Phase 3: Launching and using CertifID EMD payments

Ready to see how simple earnest money collection can be? This 30-second overview shows exactly what your buyers and team will experience:

As you saw in the video, buyers can "log in with their phone, link their bank, and send funds in minutes" while you gain complete visibility into every transaction. Here's how the dashboard featured in that demo transforms your daily operations:

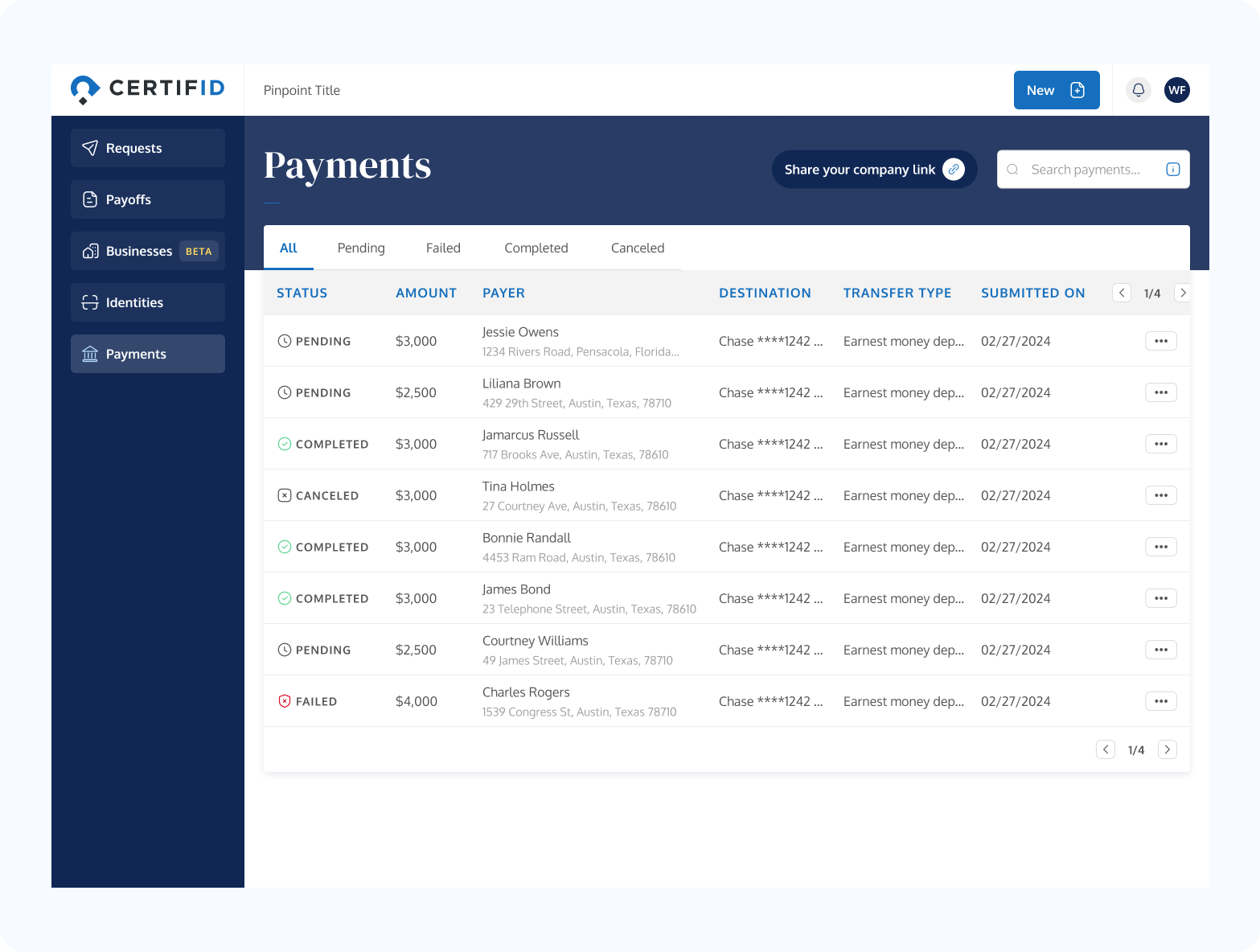

Track every EMD in one place: the Payments dashboard is the command center for escrow teams. You’ll have visibility into every transaction -status, amount, payer, destination account, and expected delivery date. Use filters to sort by buyer name, property address, payment amount, or date.

Eliminate payment confusion: Once a payment link is shared, buyers follow a few guided steps to submit their deposit. There's no app to download, no login credentials to remember, and no wire instructions to fumble. Everything happens in a secure browser session.

Connect escrow accounts securely: bank accounts are linked by your admin team. Setup is simple—just enter routing and account info, assign to an office, and validate.

Enable agents and reduce support tickets: Real estate agents often act as the bridge between buyer and title company. CertifID empowers them with an easy-to-share branded link and clear steps—no guesswork required. That means fewer calls like, "Where do I send the money?" and more time spent closing deals.

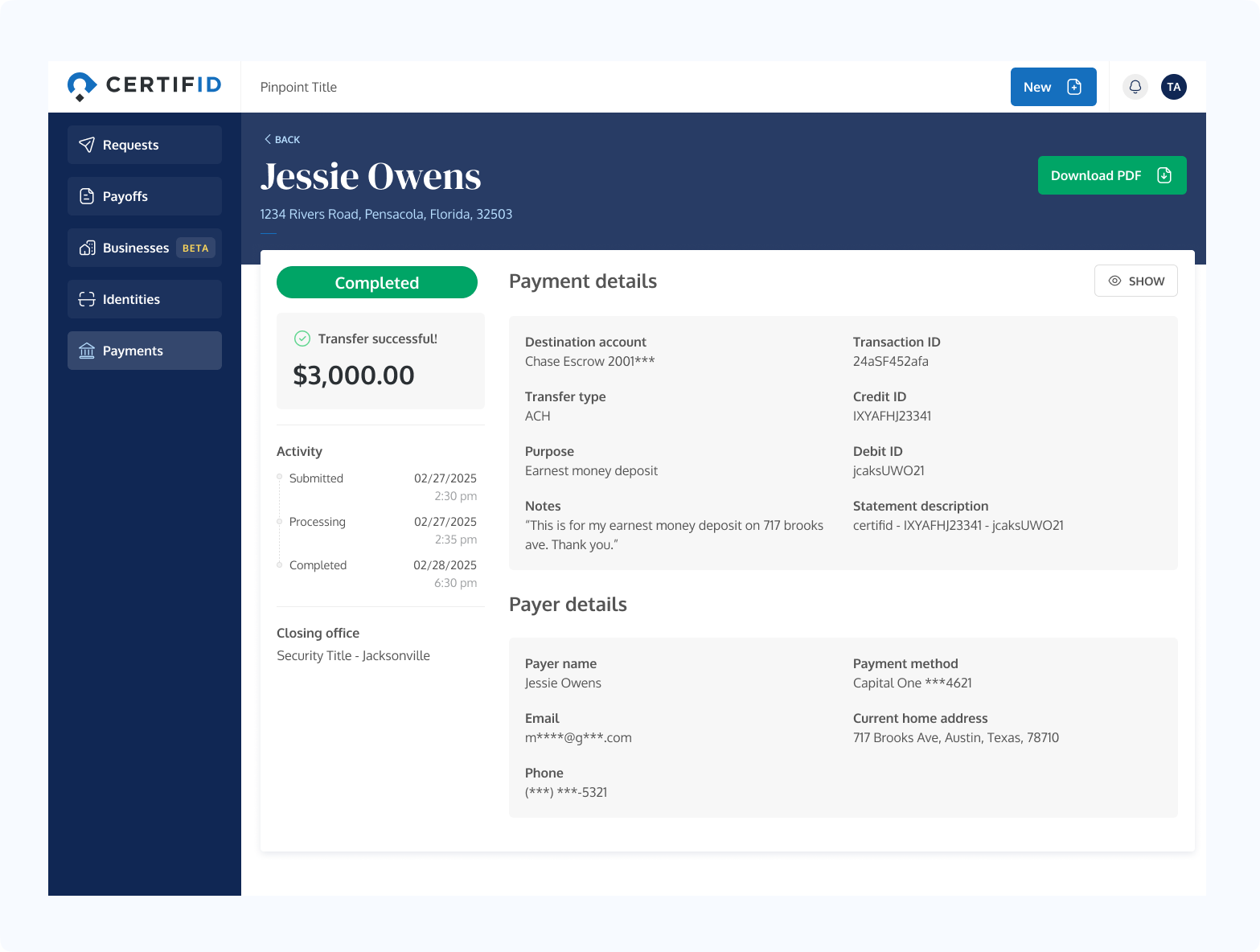

Maintain clear audit trails: Every payment includes a full record of activity: timestamps, transaction ID, payer details, and metadata. Receipts are downloadable directly from the payment view, making it easy to document for compliance or upload to your title production system.

Phase 4: Client and agent education

Train the agents who move deals forward: Host short walkthroughs or provide sharable agent kits that explain what CertifID is, how the portal works, and why it protects their clients.

Here's a quick walkthrough to share with home buyers:

Simplify buyer communications: CertifID provides buyers with a mobile-friendly experience and clear guidance.

Offer proactive support: During onboarding, ensure your team knows how to escalate questions or issues. CertifID offers email, phone, and live chat support for buyers and teams.

Capture feedback: Ask agents and buyers what worked—and what confused them. Use those insights to streamline future rollouts.

Earnest money transfer: Do it safely in your title agency

Digital earnest money solutions provide the security, transparency, speed, and compliance that modern title companies need to protect clients and stay competitive in an increasingly dangerous fraud environment.

Wire fraud risks make traditional methods increasingly dangerous. Title companies can no longer rely on outdated security measures that put client funds and business reputation at risk. The 400% increase in check fraud since the pandemic shows that manual verification procedures aren't keeping pace with criminal sophistication.

Start by mapping your current EMD process and identifying where manual steps create risk. Then evaluate modern platforms that meet your state’s compliance rules and offer built-in fraud protection. Delaying adoption increases fraud risk and puts you at a competitive disadvantage, especially as buyers increasingly expect digital payment options.

Protect your escrow accounts, reduce operational friction, and give buyers a secure, predictable way to pay. Request a CertifID demo to see how secure, compliant EMD collection works in practice.

FAQ

Senior Product Manager

Cheryl brings nearly a decade of product management experience in the real estate industry, making her mark at both scrappy startups and well-established companies. Driven by a deep customer focus and love for technology, she’s helped build innovative solutions that keep pace with evolving needs. At CertifID, Cheryl is helping drive the next phase of growth and push forward the mission to create a world without wire fraud.

Safe earnest money transfers for title companies

Cybercrime losses reported to the FBI Internet Crime Complaint Center (IC3) have grown every year, reaching $16.6 billion in 2024.

Imagine a realistic threat: A fraudster intercepts an earnest money check from an overnight drop box using a washer attached to a fishing line. They then use AI-powered check washing techniques to alter the payee and amount. The earnest money deposit (EMD) gets redirected to the criminals' account, appearing completely legitimate.

Check fraud has increased nearly 400% since 2023. Traditional earnest money transfer methods now expose title companies to fraud and compliance risks daily, with similar attacks targeting real estate professionals across the country.

This guide explains how to implement secure, compliant earnest money transfers that protect your clients, your escrow accounts, and your reputation without slowing down your closing process.

What is earnest money?

Earnest money is a good-faith deposit that demonstrates a buyer's serious intent to purchase a property. It's typically held in escrow by a title company.

This deposit creates legal obligations for both parties and shows the seller that the buyer has the financial capacity to complete the transaction.

Earnest money typically ranges from 1-10% of the purchase price, varying by local market conditions and property value.

In competitive markets, buyers often offer higher earnest money deposits to strengthen their offers. The funds are typically due within 24-72 hours of contract acceptance, creating time pressure that fraudsters exploit.

Title companies have a legal obligation to safeguard these funds in securely maintained escrow accounts. Failing to do so can result in regulatory violations, underwriting issues, and professional liability exposure.

Earnest money by state: why good funds matter

Earnest money handling requirements vary by state. Some states enforce strict good funds laws, while others rely more heavily on fiduciary standards and professional judgment. While what’s compliant in one state may violate regulations in another, modern payment platforms have evolved to make it possible to deliver earnest money digitally without sacrificing good funds compliance or exposing escrow to reversals.

Georgia requires strict compliance with good funds laws, meaning ACH transfers are not acceptable for earnest money deposits. Title professionals must verify that deposits meet the state's certified funds requirements through wire transfers or cashier's checks.

Alabama offers more discretion, as it does not have a formal good funds statute. Title professionals are expected to rely on fiduciary duty and professional standards to determine acceptable payment methods.

For title companies operating across jurisdictions, compliance can get complicated. A secure digital payment platform with configurable workflows helps simplify the process. It reduces manual oversight and supports consistent adherence to local regulations.

Why security matters

Most earnest money transfer methods are irreversible once completed, making fraud prevention more critical than recovery. Unlike credit card chargebacks, wire transfers and certified funds can't be "undone" once fraudsters receive them. This makes your verification procedures the last line of defense against financial loss.

Major risks and vulnerabilities in earnest money transfers

Wire fraud schemes

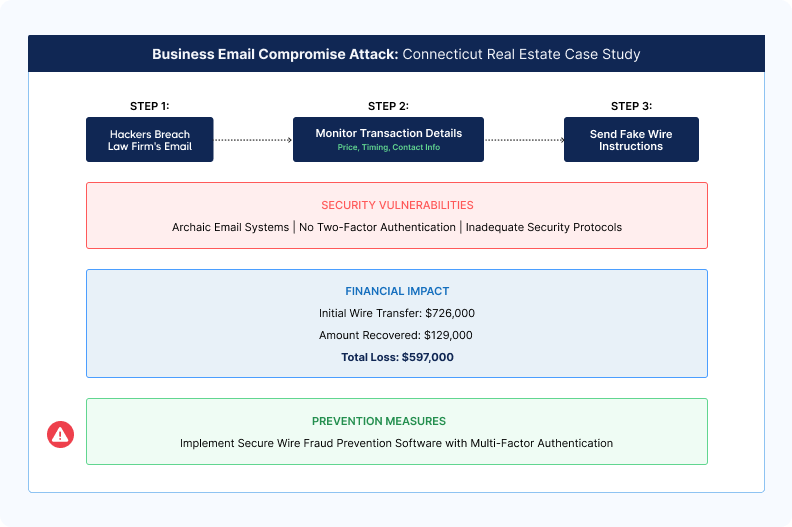

Business Email Compromise (BEC): Criminals infiltrate email accounts to intercept and modify legitimate wire instructions, often making subtle changes to routing numbers or account details.

These attacks are sophisticated and can compromise even tech-savvy professionals who think they're following secure procedures.

EMD cancellation scams: Fraudsters send large deposits via cheque (often for amounts exceeding typical EMD, like $175,000 for a $150,000 property), then quickly cancel the transaction, citing contingencies like failed inspections or zoning issues.

They request wire refunds before the original check clears, leaving title companies liable when the check bounces. This scheme specifically targets vacant land transactions and involves impersonating both listing and buying agents to appear legitimate.

Traditional method weaknesses

Each traditional payment method creates specific vulnerabilities that fraudsters exploit.

Personal checks

Check fraud is on the rise, with fraudsters using AI-powered techniques to create convincing forgeries.

Even certified checks can be fraudulent—fraudsters can intercept checks from overnight drop boxes using simple tools like washers on fishing line, then alter them using advanced check washing methods.

Our founder, Tom, experienced this firsthand in 2015.

His title company received a certified check for $180,000 that looked completely legitimate: genuine watermarks, security features, everything. Their business banker assured them it had cleared. They wired the refunds as requested, but the check was actually fraudulent and bounced days later after the wire was already sent.

The problem? Even certified checks can be sophisticated forgeries, and there's no consistent federal standard for verification across clearing houses. The clearing time window, where checks appear cleared but haven’t fully processed, creates a dangerous gap that fraudsters exploit. A secure, verified digital transfer eliminates this uncertainty.

For a detailed discussion of these check fraud tactics and how they've evolved with AI technology, watch our recent webinar "To Catch a Fraudster: Digital vs. Check Payments" where Tom and our payments expert Jason Campbell break down real-world fraud scenarios.

Wire transfers

Traditional wire transfers rely on emailed instructions that are easily spoofed or intercepted. Once sent, wires are nearly impossible to recover if they go to the wrong account.

Digital payment workflows can replace emailed instructions with secure, authenticated requests, eliminating this point of vulnerability and providing instant confirmation for all parties.

ACH transfers

ACH transfers can be reversed for up to 60 days in some cases, making them problematic for earnest money in states with good funds laws. Many states don't recognize ACH transfers as acceptable EMD deposits, creating compliance violations that can result in regulatory action.

That said, not all ACH transfers are created equal; modern digital payment platforms address these risks by verifying buyer identity, validating bank account ownership, and performing balance checks before funds are debited.

These layered controls reduce fraud, prevent unauthorized debits, and ensure payments are only initiated from verified accounts. Combined with controlled delivery and risk management, these platforms may offer compliant alternatives to traditional ACH.

Email vulnerabilities

Unencrypted email communications and account takeovers make traditional communication methods inherently unsafe for financial instructions.

Without centralized visibility of incoming payments, title companies often struggle to reconcile transactions. Modern platforms centralize payment data in one place, reducing manual matching errors and ensuring funds are quickly tied to the correct file.

Secure earnest money handling: 3 best practices

Protecting earnest money requires layered security that addresses both technical vulnerabilities and human error factors.

1. Identity verification protocols

Multi-factor authentication: Verify buyer identity through multiple independent channels—not just relying on email communications or phone calls. Fraudsters often compromise multiple communication methods simultaneously, so single-point verification creates dangerous vulnerabilities.

Document verification: Validate driver's licenses and other identification documents, checking for signs of forgery or alteration. Sophisticated fraudsters can create convincing fake IDs that pass visual inspection, so automated verification systems provide better detection rates.

Red flag identification: Watch for suspicious transaction indicators like rushed timelines, unusual payment methods, out-of-state parties with local properties, or buyers who resist verification procedures.

2. Written procedures and staff training

Standardized workflows: Document step-by-step verification processes that all staff must follow consistently. Ad-hoc procedures create vulnerabilities that fraudsters exploit, especially during busy periods when teams take shortcuts.

Annual training requirements: Provide regular staff education about evolving fraud tactics and new security threats. Fraudsters constantly adapt their methods, so training must keep pace with emerging schemes.

Escalation procedures: Define when staff should flag suspicious transactions and involve supervisors or security specialists in verification decisions. Junior staff shouldn't make security decisions alone, especially for high-value or unusual transactions.

Documentation standards: Maintain a clear audit trail that demonstrates verification procedures are strictly followed—for compliance and in the event of fraud investigations.

3. Technology security measures

Encrypted communications limitations: Even secure email isn't enough protection because BEC attacks take over entire email accounts, allowing fraudsters to send and receive emails that appear completely legitimate.

Secure payment platforms: Modern solutions like CertifID eliminate email-based wire instructions by providing secure, authenticated payment links that create trust from the outset.

Processing earnest money deposits within the same portal as other CertifID services ensures secure oversight and builds in fraud protection from day one.

Secure payment platforms remove the human error factor from instruction handling and provide tamper-proof payment processes. Compared to old-school methods, digital solutions guarantee safer transactions.

Real-time monitoring: Transaction tracking and alert systems provide immediate notification of unusual activity or failed verification attempts.

Digital payment solutions for earnest money transfers: Implementation guide

The risks and limitations of traditional payment methods highlight why secure digital platforms are becoming the new standard. Here's how they compare:

Transitioning from traditional payment methods to secure digital platforms is easier than many title companies expect, and it’s quickly becoming the industry standard for compliance and client experience.

Here’s a breakdown of the key phases involved in implementing a digital earnest money transfer solution.

Phase 1: Assessment and planning

Audit your current workflow: Start by mapping how earnest money deposits are currently collected. Identify friction points, gaps in documentation, and any exposure to manual errors or impersonation fraud.

Quantify the risk: Assess the number and average value of monthly EMD transactions. How much time does your team spend managing reconciliation for bounced checks and chasing down wire payments? This creates a baseline for improvement and a case for stakeholders.

Evaluate modern options: Look for platforms that reduce liability and manual overhead while improving the client experience. CertifID offers onboarding, SOC 2-compliant infrastructure, and direct insurance up to $5 million per file.

Budget with intention: Weigh fraud prevention and workflow efficiency against the potential cost of a single lost deposit. CertifID keeps onboarding light, requiring no extra tools or IT investment.

Secure buy-in: Present the shift as a competitive advantage. Emphasize protection, speed, and simplicity—not just for your team, but for agents and clients, too.

Phase 2: Platform selection and setup

Vendor evaluation criteria: Prioritize solutions with strong security credentials and real-time tracking.

Security validation: Verify encryption standards, identity verification protocols, and other security features that protect against fraud and ensure compliance with relevant regulations.

Phase 3: Launching and using CertifID EMD payments

Ready to see how simple earnest money collection can be? This 30-second overview shows exactly what your buyers and team will experience:

As you saw in the video, buyers can "log in with their phone, link their bank, and send funds in minutes" while you gain complete visibility into every transaction. Here's how the dashboard featured in that demo transforms your daily operations:

Track every EMD in one place: the Payments dashboard is the command center for escrow teams. You’ll have visibility into every transaction -status, amount, payer, destination account, and expected delivery date. Use filters to sort by buyer name, property address, payment amount, or date.

Eliminate payment confusion: Once a payment link is shared, buyers follow a few guided steps to submit their deposit. There's no app to download, no login credentials to remember, and no wire instructions to fumble. Everything happens in a secure browser session.

Connect escrow accounts securely: bank accounts are linked by your admin team. Setup is simple—just enter routing and account info, assign to an office, and validate.

Enable agents and reduce support tickets: Real estate agents often act as the bridge between buyer and title company. CertifID empowers them with an easy-to-share branded link and clear steps—no guesswork required. That means fewer calls like, "Where do I send the money?" and more time spent closing deals.

Maintain clear audit trails: Every payment includes a full record of activity: timestamps, transaction ID, payer details, and metadata. Receipts are downloadable directly from the payment view, making it easy to document for compliance or upload to your title production system.

Phase 4: Client and agent education

Train the agents who move deals forward: Host short walkthroughs or provide sharable agent kits that explain what CertifID is, how the portal works, and why it protects their clients.

Here's a quick walkthrough to share with home buyers:

Simplify buyer communications: CertifID provides buyers with a mobile-friendly experience and clear guidance.

Offer proactive support: During onboarding, ensure your team knows how to escalate questions or issues. CertifID offers email, phone, and live chat support for buyers and teams.

Capture feedback: Ask agents and buyers what worked—and what confused them. Use those insights to streamline future rollouts.

Earnest money transfer: Do it safely in your title agency

Digital earnest money solutions provide the security, transparency, speed, and compliance that modern title companies need to protect clients and stay competitive in an increasingly dangerous fraud environment.

Wire fraud risks make traditional methods increasingly dangerous. Title companies can no longer rely on outdated security measures that put client funds and business reputation at risk. The 400% increase in check fraud since the pandemic shows that manual verification procedures aren't keeping pace with criminal sophistication.

Start by mapping your current EMD process and identifying where manual steps create risk. Then evaluate modern platforms that meet your state’s compliance rules and offer built-in fraud protection. Delaying adoption increases fraud risk and puts you at a competitive disadvantage, especially as buyers increasingly expect digital payment options.

Protect your escrow accounts, reduce operational friction, and give buyers a secure, predictable way to pay. Request a CertifID demo to see how secure, compliant EMD collection works in practice.

Senior Product Manager

Cheryl brings nearly a decade of product management experience in the real estate industry, making her mark at both scrappy startups and well-established companies. Driven by a deep customer focus and love for technology, she’s helped build innovative solutions that keep pace with evolving needs. At CertifID, Cheryl is helping drive the next phase of growth and push forward the mission to create a world without wire fraud.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503