Workflow automation in real estate: Guide for escrow managers & closing attorneys

Real estate teams don’t struggle from a lack of tools—they struggle with fragmented workflows that add risk. This guide shows where automation helps escrow teams and closing attorneys—and where it creates problems.

Share article:

Katie Stewart

8 minutes

Education

Feb 11, 2026

Feb 11, 2026

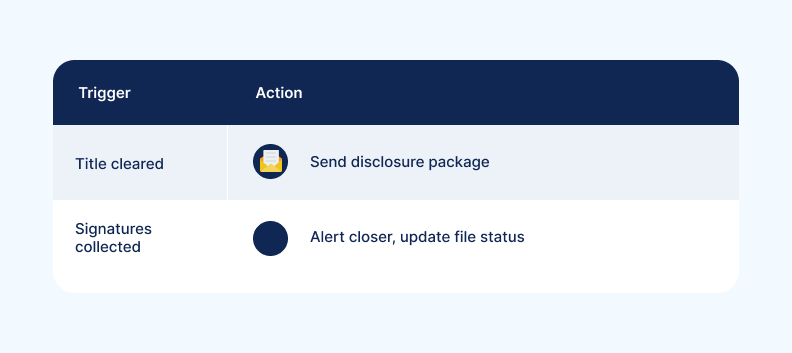

Workflow automation uses triggers to initiate actions automatically—a new escrow file opens and a welcome packet is sent; a title clears and an e-signature request fires.

For agents, automation means faster lead response. For escrow teams and closing attorneys, it means fewer manual callbacks, less double data entry, and tighter security on wire transfers.

This guide covers key automation areas across real estate, with deeper focus on escrow and closing workflows where the stakes are highest.

What is workflow automation in real estate?

Workflow automation is technology that performs repetitive tasks automatically based on triggers and conditions. A form submission triggers a CRM update. A document signature triggers the next step in a closing checklist.

Here's how automation applies differently across real estate roles:

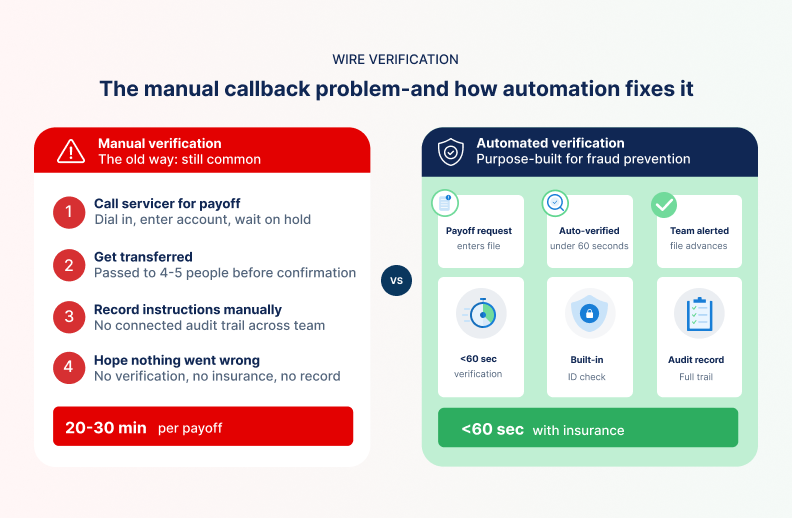

Automation matters now because fraudsters use AI to scale attacks. Manual processes can't keep pace. According to our data, wire fraud losses average $68K-$276K per incident, depending on transaction type. The manual callback that worked in 2015 isn't sufficient protection in 2026.

Key areas for workflow automation

Automation touches every stage of real estate, from first client contact to post-closing follow-up. This section breaks down the key areas, starting with agent-focused workflows before diving deeper into escrow and closing operations.

Lead generation and management

Automation can capture leads from Zillow, Realtor.com, or Facebook, route them into a CRM, and assign based on criteria like location or price range. The goal is immediate response—no lead sits unanswered while an agent finishes a showing.

Lead nurturing

Trigger-based sequences keep prospects engaged: a buyer favorites a property and receives comparable listings; a seller downloads a home valuation and enters a nurture campaign. This maintains engagement without requiring manual follow-up on every interaction.

Transaction and document management

For escrow and title workflows, automation generates contracts, disclosures, and closing documents from title production software, then triggers e-signature requests when milestones are hit.

Files move from order opener to processor to closer, but handoffs are often unclear. Some teams pass physical files, some use shared email, and others rely on inconsistent checklists.

One operations manager noted her team needs files "one week before closing fully processed"—but with manual processes, that rarely happens. Automation creates visibility across the entire file lifecycle.

Client onboarding

Automated welcome packets, document checklists, and intake forms deliver what clients need immediately.

For escrow teams, this includes KYC collection and wire instruction requests. For agents, buyer/seller questionnaires. The key benefit: clients receive what they need without staff manually sending each item.

Scheduling and follow-up

Auto-scheduling closings when clear-to-close arrives, sending reminders at 48 hours, 24 hours, and day-of, then triggering post-closing follow-ups keeps files moving.

Lenders frequently don't deliver final loan packages until hours before closing—sometimes day-of. One escrow officer noted that 80% of her business involves remote closings with mobile notaries, and lender delays create enormous pressure.

Automation can't fix lender timing, but it eliminates every other bottleneck so teams are ready the moment documents arrive.

Wire verification and fund movement

Manual payoff verification takes 20-30 minutes per callback—sometimes getting transferred to four or five people before reaching someone who can confirm instructions. Wire instruction collection via email creates direct fraud exposure.

Automation replaces:

- Manual payoff verification (20-30 minute callbacks) with automated payoff verification in under 60 seconds

- Email-based wire instruction sharing with secure collection featuring built-in identity verification

- Delayed fund confirmations with real-time alerts when funds arrive or issues arise

As an escrow officer, you might be spending 16+ hours monthly on manual tasks. Current solutions can help you save that time so you can spend more time on high-value tasks and building industry relationships.

Benefits of workflow automation

When implemented well, automation delivers measurable gains across productivity, speed, accuracy, and growth capacity. Here's what title companies and law firms can expect.

Reduced human error

Manual processes also leave room for silent handoffs. One team member verifies wiring instructions over the phone, another sends the wire, and a third records the file—but none of that context is connected.

When something goes wrong, there’s no clear record of who verified what, when, or based on which source. Automation ties identity verification, instruction collection, and confirmation into a single system of record, creating a defensible audit trail that holds up under review.

Faster response times

Instant verification keeps files moving. Manual callbacks create bottlenecks—one escrow officer described payoff calls to servicers like Mr. Cooper taking "20, 30 minutes... passed to four or five different people before you get someone who can actually confirm."

Increased productivity

Teams report completing a week's worth of payoff verifications in minutes. One early adopter of automated payoff verification said she now has "my whole week done in a matter of minutes." Across the industry, automated tools may save an estimated 38,000+ employee hours.

Scalability

Small teams handle higher volume without adding headcount. A 4-person law firm can manage closings that previously required dedicated processors. A title company processing 300+ monthly closings can maintain consistency across all files.

Competitive differentiation

According to our data, 79% of consumers are willing to pay more to work with a real estate business that prioritizes security. Position automation as a selling point for winning enterprise accounts and referral partners.

Real estate workflow automation: Common drawbacks and challenges

Automation isn't a silver bullet. Implementation comes with real challenges—from integration headaches to client resistance. Understanding these pitfalls helps avoid them.

Tool sprawl and integration failures

Some solutions are designed to operate primarily within a single ecosystem. While this can simplify certain workflows, it can also limit flexibility when teams need to layer in specialized tools.

One operations manager described paying for a platform feature that clients rarely use, then reverting to Outlook to move transactions forward—creating double data entry. Adding another tool on top turns that into triple entry. “We’re paying for something that isn’t being used,” she said. “And it isn’t actually protecting us from payment fraud.”

In these environments, firms are often forced to choose between ecosystem convenience and best-in-class point solutions—streamlined workflows on paper versus meaningful verification and protection against fraud in practice.

Client adoption resistance

Portal-based solutions often face adoption challenges. Clients don't want another login, don't trust entering bank credentials into unfamiliar systems, or simply ignore requests.

One escrow manager noted that asking clients to log into a portal and then into their bank feels like "everything we educate people not to do." The result: staff end up chasing clients manually anyway, negating the automation benefit.

Automation without protection

Some tools automate communication—sending secure-looking emails and tracking document status—but don't actually verify wire instructions, validate identities, or provide fraud insurance backing.

Faster file movement without fraud detection just accelerates risk. Some verification tools have low success rates (40-70%) and lack clear insurance protections, leaving firms exposed even when they think they're covered.

Implementation complexity

Mapping workflows, training teams, and building automation rules takes effort. Without proper setup, automation creates new problems—wrong triggers, missed steps, alerts that get ignored. Start small and expand methodically.

Popular tools for real estate workflow automation

The right tools depend on your role and existing systems. This section covers options for both agent-side and transaction-side automation, plus key criteria for making selections.

For agents and brokerages

- CRM systems: Follow Up Boss, Lofty (formerly Chime), Salesforce—for lead tracking and pipeline management

- No-code workflow tools: Zapier, Make—for connecting systems that don't natively integrate

- Form and document tools: Docusign—for e-signatures and transaction coordination

For title companies, escrow teams, and attorneys

- Title production software: SoftPro, ResWare, Qualia, RamQuest—the foundation systems where other tools integrate

- E-signatures: Docusign—integrates with most TPS (and soon CertifID)

- Wire fraud prevention: CertifID—payoff verification, identity verification, secure wire sharing; partners with major underwriters (Old Republic, Stewart)

The key distinction in the verification category: some tools were built as workflow platforms and added security features later, while others were purpose-built for fraud prevention from the start.

This affects verification depth, support quality (whether you get callbacks on unable-to-verify results), and insurance structure (first-party direct coverage vs. third-party claims processes).

What to prioritize when selecting tools

- Direct native integration and API connections with existing title production software

- Tools that replace workflows rather than add logins

- Insurance-backed solutions for wire verification—look for first-party coverage with clear claims processes

- Non-invasive client experience—avoid solutions requiring bank credential entry or SSN collection when simpler verification methods exist

What to avoid

- Tools requiring app downloads that clients won't install

- Solutions that create additional data entry rather than reducing it

- "Automation" that sends notifications but doesn't actually verify or protect

How to implement workflow automation

Successful implementation starts with understanding your current state, then building incrementally.

This four-step process works for both small firms and multi-office operations.

Step 1: Map current workflows

Start by identifying where manual effort concentrates. Track one week of closings and note every touchpoint where staff re-key data, chase follow-ups, or wait on handoffs.

Common bottlenecks to look for:

- Payoff verification (phone callbacks to lenders)

- Wire instruction collection (email back-and-forth)

- Document status tracking (manually checking what's signed—a lot of back-and-forth)

- Closing scheduling (coordinating multiple calendars)

Ask: "Where do files stall between people, and why?"

Step 2: Prioritize by impact and risk

Start where stakes are highest. For escrow managers, wire verification combines significant fraud exposure with major time drain—it's the natural starting point.

For attorneys handling high-risk transactions (out-of-state sellers, vacant land, LLC buyers), identity verification addresses the biggest liability concern.

Operations managers or IT directors should typically own this implementation process, working with closers and processors to identify priorities.

Step 3: Select and integrate tools

- Audit what your title production software already offers

- Identify gaps—particularly in verification, fraud prevention, and payments

- Choose tools with native integrations rather than relying on workarounds for critical processes

Example: Escrow manager workflow: SoftPro + automated payoff verification → Payoff received → Submit to verification engine → Verified in 60 seconds → Team alerted → File moves forward

Example: Closing attorney workflow: SoftPro + identity verification → High-risk seller identified → Send verification request → Results returned with insurance backing → Proceed or flag for review

Step 4: Pilot, measure, and scale

Start with one workflow, run it for 30 days, and track results before expanding.

Metrics to monitor:

- Time-to-close improvement

- Callbacks eliminated per week

- Staff hours recovered

- Fraud attempts caught or flagged

Don't automate everything at once. Get one workflow running smoothly, then add the next priority area.

Workflows in real estate: Modernize your company and win the market

Workflow automation eliminates manual processes that create delays, errors, and fraud exposure.

For agents, faster lead response. For escrow teams and attorneys, replacing the callback-and-chase cycle with integrated verification.

Start with the highest-risk, highest-time-drain workflows, measure the results, and scale from there.

Subscribe to our newsletter for more tips on how to optimize operations in your title company.

FAQ

Why do some "smart tasks" feel like more work, not less?

Because they add tasks rather than replace them. True automation should eliminate manual steps—like automatically sending payoff requests—not just create another checklist item. If you're still doing callbacks and double entry, you're not actually automated.

How do I handle file handoffs between the processor and the closer?

Most teams use a combination of shared email, file checklists, and clear triggers (e.g., file moves to a closer when the CD is received for balancing). Cross-training helps smaller teams stay flexible. The key: everyone should know what's done and what's pending without asking.

What if clients won't use the automation tools we send them?

This is common. Some clients refuse portals, ignore requests, or distrust entering bank credentials. The solution: choose tools with non-invasive verification (no logins or SSN required), offer manual alternatives for resistant clients, and treat refusal itself as a red flag worth noting.

Does workflow automation in real estate replace staff?

No—it frees staff from repetitive tasks to focus on complex files, curative issues, and client relationships. Teams handling 300+ closings monthly need automation to maintain quality, not to cut headcount.

VP of Customer Success

Katie's background combines both IT and education. Her degree is in Management Information Systems, and she spent her first four years in the workforce as an IT business analyst. Katie took a career turn and joined Teach for America and worked in inner-city schools in Indianapolis as a math teacher and eventually an assistant principal. Today she combines her IT nerdiness and love of teaching, helping customers find success every day.

Workflow automation uses triggers to initiate actions automatically—a new escrow file opens and a welcome packet is sent; a title clears and an e-signature request fires.

For agents, automation means faster lead response. For escrow teams and closing attorneys, it means fewer manual callbacks, less double data entry, and tighter security on wire transfers.

This guide covers key automation areas across real estate, with deeper focus on escrow and closing workflows where the stakes are highest.

What is workflow automation in real estate?

Workflow automation is technology that performs repetitive tasks automatically based on triggers and conditions. A form submission triggers a CRM update. A document signature triggers the next step in a closing checklist.

Here's how automation applies differently across real estate roles:

Automation matters now because fraudsters use AI to scale attacks. Manual processes can't keep pace. According to our data, wire fraud losses average $68K-$276K per incident, depending on transaction type. The manual callback that worked in 2015 isn't sufficient protection in 2026.

Key areas for workflow automation

Automation touches every stage of real estate, from first client contact to post-closing follow-up. This section breaks down the key areas, starting with agent-focused workflows before diving deeper into escrow and closing operations.

Lead generation and management

Automation can capture leads from Zillow, Realtor.com, or Facebook, route them into a CRM, and assign based on criteria like location or price range. The goal is immediate response—no lead sits unanswered while an agent finishes a showing.

Lead nurturing

Trigger-based sequences keep prospects engaged: a buyer favorites a property and receives comparable listings; a seller downloads a home valuation and enters a nurture campaign. This maintains engagement without requiring manual follow-up on every interaction.

Transaction and document management

For escrow and title workflows, automation generates contracts, disclosures, and closing documents from title production software, then triggers e-signature requests when milestones are hit.

Files move from order opener to processor to closer, but handoffs are often unclear. Some teams pass physical files, some use shared email, and others rely on inconsistent checklists.

One operations manager noted her team needs files "one week before closing fully processed"—but with manual processes, that rarely happens. Automation creates visibility across the entire file lifecycle.

Client onboarding

Automated welcome packets, document checklists, and intake forms deliver what clients need immediately.

For escrow teams, this includes KYC collection and wire instruction requests. For agents, buyer/seller questionnaires. The key benefit: clients receive what they need without staff manually sending each item.

Scheduling and follow-up

Auto-scheduling closings when clear-to-close arrives, sending reminders at 48 hours, 24 hours, and day-of, then triggering post-closing follow-ups keeps files moving.

Lenders frequently don't deliver final loan packages until hours before closing—sometimes day-of. One escrow officer noted that 80% of her business involves remote closings with mobile notaries, and lender delays create enormous pressure.

Automation can't fix lender timing, but it eliminates every other bottleneck so teams are ready the moment documents arrive.

Wire verification and fund movement

Manual payoff verification takes 20-30 minutes per callback—sometimes getting transferred to four or five people before reaching someone who can confirm instructions. Wire instruction collection via email creates direct fraud exposure.

Automation replaces:

- Manual payoff verification (20-30 minute callbacks) with automated payoff verification in under 60 seconds

- Email-based wire instruction sharing with secure collection featuring built-in identity verification

- Delayed fund confirmations with real-time alerts when funds arrive or issues arise

As an escrow officer, you might be spending 16+ hours monthly on manual tasks. Current solutions can help you save that time so you can spend more time on high-value tasks and building industry relationships.

Benefits of workflow automation

When implemented well, automation delivers measurable gains across productivity, speed, accuracy, and growth capacity. Here's what title companies and law firms can expect.

Reduced human error

Manual processes also leave room for silent handoffs. One team member verifies wiring instructions over the phone, another sends the wire, and a third records the file—but none of that context is connected.

When something goes wrong, there’s no clear record of who verified what, when, or based on which source. Automation ties identity verification, instruction collection, and confirmation into a single system of record, creating a defensible audit trail that holds up under review.

Faster response times

Instant verification keeps files moving. Manual callbacks create bottlenecks—one escrow officer described payoff calls to servicers like Mr. Cooper taking "20, 30 minutes... passed to four or five different people before you get someone who can actually confirm."

Increased productivity

Teams report completing a week's worth of payoff verifications in minutes. One early adopter of automated payoff verification said she now has "my whole week done in a matter of minutes." Across the industry, automated tools may save an estimated 38,000+ employee hours.

Scalability

Small teams handle higher volume without adding headcount. A 4-person law firm can manage closings that previously required dedicated processors. A title company processing 300+ monthly closings can maintain consistency across all files.

Competitive differentiation

According to our data, 79% of consumers are willing to pay more to work with a real estate business that prioritizes security. Position automation as a selling point for winning enterprise accounts and referral partners.

Real estate workflow automation: Common drawbacks and challenges

Automation isn't a silver bullet. Implementation comes with real challenges—from integration headaches to client resistance. Understanding these pitfalls helps avoid them.

Tool sprawl and integration failures

Some solutions are designed to operate primarily within a single ecosystem. While this can simplify certain workflows, it can also limit flexibility when teams need to layer in specialized tools.

One operations manager described paying for a platform feature that clients rarely use, then reverting to Outlook to move transactions forward—creating double data entry. Adding another tool on top turns that into triple entry. “We’re paying for something that isn’t being used,” she said. “And it isn’t actually protecting us from payment fraud.”

In these environments, firms are often forced to choose between ecosystem convenience and best-in-class point solutions—streamlined workflows on paper versus meaningful verification and protection against fraud in practice.

Client adoption resistance

Portal-based solutions often face adoption challenges. Clients don't want another login, don't trust entering bank credentials into unfamiliar systems, or simply ignore requests.

One escrow manager noted that asking clients to log into a portal and then into their bank feels like "everything we educate people not to do." The result: staff end up chasing clients manually anyway, negating the automation benefit.

Automation without protection

Some tools automate communication—sending secure-looking emails and tracking document status—but don't actually verify wire instructions, validate identities, or provide fraud insurance backing.

Faster file movement without fraud detection just accelerates risk. Some verification tools have low success rates (40-70%) and lack clear insurance protections, leaving firms exposed even when they think they're covered.

Implementation complexity

Mapping workflows, training teams, and building automation rules takes effort. Without proper setup, automation creates new problems—wrong triggers, missed steps, alerts that get ignored. Start small and expand methodically.

Popular tools for real estate workflow automation

The right tools depend on your role and existing systems. This section covers options for both agent-side and transaction-side automation, plus key criteria for making selections.

For agents and brokerages

- CRM systems: Follow Up Boss, Lofty (formerly Chime), Salesforce—for lead tracking and pipeline management

- No-code workflow tools: Zapier, Make—for connecting systems that don't natively integrate

- Form and document tools: Docusign—for e-signatures and transaction coordination

For title companies, escrow teams, and attorneys

- Title production software: SoftPro, ResWare, Qualia, RamQuest—the foundation systems where other tools integrate

- E-signatures: Docusign—integrates with most TPS (and soon CertifID)

- Wire fraud prevention: CertifID—payoff verification, identity verification, secure wire sharing; partners with major underwriters (Old Republic, Stewart)

The key distinction in the verification category: some tools were built as workflow platforms and added security features later, while others were purpose-built for fraud prevention from the start.

This affects verification depth, support quality (whether you get callbacks on unable-to-verify results), and insurance structure (first-party direct coverage vs. third-party claims processes).

What to prioritize when selecting tools

- Direct native integration and API connections with existing title production software

- Tools that replace workflows rather than add logins

- Insurance-backed solutions for wire verification—look for first-party coverage with clear claims processes

- Non-invasive client experience—avoid solutions requiring bank credential entry or SSN collection when simpler verification methods exist

What to avoid

- Tools requiring app downloads that clients won't install

- Solutions that create additional data entry rather than reducing it

- "Automation" that sends notifications but doesn't actually verify or protect

How to implement workflow automation

Successful implementation starts with understanding your current state, then building incrementally.

This four-step process works for both small firms and multi-office operations.

Step 1: Map current workflows

Start by identifying where manual effort concentrates. Track one week of closings and note every touchpoint where staff re-key data, chase follow-ups, or wait on handoffs.

Common bottlenecks to look for:

- Payoff verification (phone callbacks to lenders)

- Wire instruction collection (email back-and-forth)

- Document status tracking (manually checking what's signed—a lot of back-and-forth)

- Closing scheduling (coordinating multiple calendars)

Ask: "Where do files stall between people, and why?"

Step 2: Prioritize by impact and risk

Start where stakes are highest. For escrow managers, wire verification combines significant fraud exposure with major time drain—it's the natural starting point.

For attorneys handling high-risk transactions (out-of-state sellers, vacant land, LLC buyers), identity verification addresses the biggest liability concern.

Operations managers or IT directors should typically own this implementation process, working with closers and processors to identify priorities.

Step 3: Select and integrate tools

- Audit what your title production software already offers

- Identify gaps—particularly in verification, fraud prevention, and payments

- Choose tools with native integrations rather than relying on workarounds for critical processes

Example: Escrow manager workflow: SoftPro + automated payoff verification → Payoff received → Submit to verification engine → Verified in 60 seconds → Team alerted → File moves forward

Example: Closing attorney workflow: SoftPro + identity verification → High-risk seller identified → Send verification request → Results returned with insurance backing → Proceed or flag for review

Step 4: Pilot, measure, and scale

Start with one workflow, run it for 30 days, and track results before expanding.

Metrics to monitor:

- Time-to-close improvement

- Callbacks eliminated per week

- Staff hours recovered

- Fraud attempts caught or flagged

Don't automate everything at once. Get one workflow running smoothly, then add the next priority area.

Workflows in real estate: Modernize your company and win the market

Workflow automation eliminates manual processes that create delays, errors, and fraud exposure.

For agents, faster lead response. For escrow teams and attorneys, replacing the callback-and-chase cycle with integrated verification.

Start with the highest-risk, highest-time-drain workflows, measure the results, and scale from there.

Subscribe to our newsletter for more tips on how to optimize operations in your title company.

VP of Customer Success

Katie's background combines both IT and education. Her degree is in Management Information Systems, and she spent her first four years in the workforce as an IT business analyst. Katie took a career turn and joined Teach for America and worked in inner-city schools in Indianapolis as a math teacher and eventually an assistant principal. Today she combines her IT nerdiness and love of teaching, helping customers find success every day.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503