ALTA Best Practices for escrow managers

Turn ALTA Best Practices into daily workflows that create proof automatically and reduce wire fraud risk.

Share article:

.png)

Michelle Artreche

8 minutes

Education

Feb 5, 2026

Feb 5, 2026

When lenders ask for documented wire fraud prevention procedures, there are only two outcomes. You either deliver clean, complete audit trails right away, or you scramble to piece together proof after the fact.

Most escrow managers know this gap. Your team follows the right procedures. They verify wire instructions. They reconcile accounts. They complete training. But when an auditor or lender asks for evidence, that proof often lives in handwritten notes, inboxes, or spreadsheets that were never meant to stand up to scrutiny.

Manual processes create documentation gaps even when everything was done correctly.

ALTA Best Practices are designed to close that gap. Not by adding more tasks, but by creating standardized operations where compliance happens systematically and proof is built into daily workflows.

Escrow managers who operationalize ALTA standards gain more than audit readiness. They answer lender questionnaires faster, pass reviews with confidence, reduce cyber insurance friction, and create consistency across locations. The shift is subtle but powerful. Moving from “we do this” to “here’s the timestamped proof” changes how compliance feels day to day.

Because confident compliance is about building systems where proof is created automatically as the work gets done. That is exactly the problem ALTA Best Practices were designed to solve.

What are ALTA Best Practices?

ALTA Best Practices is a framework developed by the American Land Title Association to standardize operations, reduce risk, and protect consumers across the title and settlement industry.

Title companies should follow these guidelines, even though they are not laws. Lenders, underwriters, and insurers expect title companies to comply with these guidelines. They often check for participation and compliance using resources like the ALTA Registry.

ALTA Best Practices define how a title or settlement company should operate across seven core areas, with an emphasis on written procedures, internal controls, and documentation that can be verified during audits.

For escrow managers, these pillars are the operational foundation for compliance and audit readiness. The framework includes seven pillars:

Pillar 1: Licensing

Maintain current licenses as required for title insurance and settlement services.

Pillar 2: Escrow trust accounting

Adopt written procedures and controls for escrow trust accounts with electronic verification of reconciliation.

Pillar 3: Protecting non-public information (NPI)

Adopt a written information security plan and privacy plan.

Pillar 4: Settlement processes

Adopt standard settlement policies ensuring compliance with federal and state consumer protection laws, including wire fraud prevention.

Pillar 5: Policy production

Maintain written procedures for title policy production, delivery, reporting, and premium remittance.

Pillar 6: Insurance coverage

Maintain appropriate professional liability, E&O, cyber liability, and crime coverage.

Pillar 7: Consumer complaints

Adopt written procedures for resolving consumer complaints.

For escrow managers, these pillars are not abstract compliance requirements. They show up in daily workflows, staff training, transaction handling, and audit preparation. Escrow managers are the operational owners responsible for implementation, consistency, and proof.

Understanding the pillars is only the starting point. The real challenge for escrow managers is not following these standards, but proving that they are followed consistently and completely.

Why audit-ready operations matter for escrow managers

The biggest risk for most escrow managers is being unable to prove compliance efficiently.

Manual processes, inconsistent documentation, and scattered records create exposure even when procedures are followed correctly. That gap becomes painful in four common situations:

- Lender questionnaires that demand documented procedures and verification logs

- SOC 2 reviews and compliance audits that require complete audit trails

- Cyber insurance renewals that need proof of security measures to avoid rate increases

- Multi-branch operations where inconsistency creates compliance gaps across locations

The shift required is fundamental. Moving from manual verification that relies on memory and notes to systematic approaches that create proof layers inside everyday workflows.

Audit-ready operations do not rely on people remembering to document. They build documentation into the process itself.

While all seven pillars matter, some create significantly more day-to-day exposure for escrow managers when audits and lender reviews occur.

ALTA best practices every escrow manager should prioritize

All seven ALTA pillars impact escrow operations, but some create more day-to-day exposure for escrow managers than others. What matters most is how each pillar shows up in real workflows and what auditors expect to see when they ask for proof.

You can reference the official ALTA Best Practices 4.2 Framework, effective August 19, 2025, for full requirements.

Pillar 1: Licensing

Title companies must establish and maintain all required licenses to conduct title insurance and settlement services.

For escrow managers, this means tracking business and individual licenses, meeting state requirements, maintaining Policy Forms Licensing compliance, and staying listed in the ALTA Registry.

Auditors look for proof that licensing is continuously monitored, including current certificates, renewal tracking with no lapses, and continuing education records. Helpful licensing resources include the NAIC State Licensing Map, ALTA Policy Forms Licensing, and the TIRS State Compliance Guide.

Pillar 2: Escrow trust accounting

Escrow trust accounting is one of the most heavily audited areas of ALTA compliance.

Requirements include properly identified trust accounts, no commingling of funds, and reconciliations that allow electronic verification.

Wire transfer procedures are central here. ALTA requires written protocols, annual testing, multi-factor authentication, and independent verification of wire instructions using secure software.

Manual callbacks and handwritten notes are common failure points. Tools like CertifID’s PayoffProtect automate verification and create timestamped audit trails. Auditors expect daily and monthly reconciliations, segregation of duties, management review, background checks, and wire fraud training.

Pillar 3: Protecting non-public information

This pillar requires a written information security plan and privacy plan to protect NPI under laws like the Gramm-Leach-Bliley Act.

Escrow managers are responsible for enforcing multi-factor authentication, password policies, access controls, and timely updates.

Proof includes access logs, encryption standards, annual security training records, incident response plans, and tested business continuity plans. Vendors with system access must align with these policies.

Additional guidance is available through the FTC Data Security Best Practices, FTC identity theft prevention guidance, and ALTA’s Business Continuity and Disaster Recovery guidance.

Pillar 4: Settlement processes (including wire fraud prevention)

Settlement processes include wire fraud prevention, the highest-risk area for escrow operations.

ALTA requires staff training, pricing controls, identity fraud prevention, and written wire transfer procedures tested annually. Response procedures should align with the ALTA Rapid Response Plan to ensure quick, coordinated action when fraud is suspected.

Auditors look for secure verification tools, multi-factor authentication, timestamped verification logs, and documented wire fraud response plans. Informal notes do not meet audit standards.

Pillar 5: Policy production

Title policies must be issued within required timeframes and reported accurately. Escrow managers must maintain written procedures, policy registers, timely reporting, and premium remittance records that demonstrate compliance.

Pillar 6: Insurance coverage

Companies must maintain appropriate E&O, cyber, and crime insurance. Proof includes current certificates, staff awareness of coverage limitations, and documented annual reviews with brokers.

Pillar 7: Consumer complaints

Written procedures must govern how complaints are received, escalated, and resolved. Auditors expect standardized forms tied to transactions, a designated point of contact, and complaint logs that track resolution.

This is where many escrow teams get stuck. They understand the requirements, but lack workflows that create audit-ready proof automatically.

How to operationalize ALTA best practices across your escrow team

The difference between compliance and audit readiness is the documentation created automatically through workflow.

Below is a simplified implementation framework.

For multi-branch operations, standardized workflows are critical. Every location must follow identical procedures. Central documentation repositories give auditors single-source access to records.

Technology that enforces protocols automatically removes reliance on memory and eliminates documentation gaps. To make this shift practical, escrow managers need a clear, time-bound plan.

Your 90-day roadmap to ALTA compliance

Month 1: Assess

Audit current workflows against all seven ALTA pillars. Identify where documentation gaps create audit risk. Review past lender questionnaires and audit findings. Survey staff to understand where processes break under pressure.

Month 2: Implement

Develop standardized procedures, starting with wire fraud prevention. Train staff using ALTA resources and real case studies. Integrate verification tools where manual processes create gaps.

Month 3: Monitor

Run an internal review using an auditor’s lens. Organize documentation so records are easy to retrieve. Establish a quarterly review cadence to keep practices current.

Getting started with ALTA Best Practices

ALTA Best Practices are the operational framework for building an escrow operation that passes audits with confidence.

Escrow managers who treat compliance as a capability, not a task, reduce insurance costs, strengthen lender relationships, and scale more efficiently.

The work starts with understanding your current state across all seven pillars. Prioritize wire fraud prevention under Pillar 4, then build systems that create proof automatically so audit readiness becomes the default, not a scramble when questions arise.

For ongoing guidance, practical compliance protocols, and real-world fraud prevention insights, subscribe to our newsletter, The Wire. You’ll get educational resources designed to help escrow teams stay protected as threats and audit expectations continue to evolve.

FAQ

Do I need to follow all seven ALTA pillars or can I prioritize certain ones?

While all seven pillars are important, you should implement all of them to achieve true ALTA compliance. However, many escrow managers start with wire fraud prevention (Pillar 4) and escrow trust accounting (Pillar 2) as the highest-risk areas, then systematically address the remaining pillars.

How often do ALTA Best Practices get updated?

ALTA regularly reviews and updates the Best Practices Framework. The current version is 4.2, effective August 19, 2025. ALTA accepts stakeholder comments and a formal committee reviews improvements on an ongoing basis, so it's important to check their website periodically for updates.

Are ALTA Best Practices legally required or just recommendations?

ALTA Best Practices are not legal requirements—they're voluntary industry standards.

However, lenders, underwriters, and cyber insurers expect compliance. Many E&O insurance policies now want to see documented verification procedures that align with ALTA standards.

What's the difference between doing ALTA compliance and proving ALTA compliance?

Doing compliance means following proper safety procedures—using secure software for payoff instruction ordering & verification, reconciling accounts, and training staff.

Proving compliance means creating systematic documentation that survives audits. It includes timestamped verification logs, signed training records, and completed reconciliation reports. The shift from manual to systematic processes ensures you can prove what you've done.

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

When lenders ask for documented wire fraud prevention procedures, there are only two outcomes. You either deliver clean, complete audit trails right away, or you scramble to piece together proof after the fact.

Most escrow managers know this gap. Your team follows the right procedures. They verify wire instructions. They reconcile accounts. They complete training. But when an auditor or lender asks for evidence, that proof often lives in handwritten notes, inboxes, or spreadsheets that were never meant to stand up to scrutiny.

Manual processes create documentation gaps even when everything was done correctly.

ALTA Best Practices are designed to close that gap. Not by adding more tasks, but by creating standardized operations where compliance happens systematically and proof is built into daily workflows.

Escrow managers who operationalize ALTA standards gain more than audit readiness. They answer lender questionnaires faster, pass reviews with confidence, reduce cyber insurance friction, and create consistency across locations. The shift is subtle but powerful. Moving from “we do this” to “here’s the timestamped proof” changes how compliance feels day to day.

Because confident compliance is about building systems where proof is created automatically as the work gets done. That is exactly the problem ALTA Best Practices were designed to solve.

What are ALTA Best Practices?

ALTA Best Practices is a framework developed by the American Land Title Association to standardize operations, reduce risk, and protect consumers across the title and settlement industry.

Title companies should follow these guidelines, even though they are not laws. Lenders, underwriters, and insurers expect title companies to comply with these guidelines. They often check for participation and compliance using resources like the ALTA Registry.

ALTA Best Practices define how a title or settlement company should operate across seven core areas, with an emphasis on written procedures, internal controls, and documentation that can be verified during audits.

For escrow managers, these pillars are the operational foundation for compliance and audit readiness. The framework includes seven pillars:

Pillar 1: Licensing

Maintain current licenses as required for title insurance and settlement services.

Pillar 2: Escrow trust accounting

Adopt written procedures and controls for escrow trust accounts with electronic verification of reconciliation.

Pillar 3: Protecting non-public information (NPI)

Adopt a written information security plan and privacy plan.

Pillar 4: Settlement processes

Adopt standard settlement policies ensuring compliance with federal and state consumer protection laws, including wire fraud prevention.

Pillar 5: Policy production

Maintain written procedures for title policy production, delivery, reporting, and premium remittance.

Pillar 6: Insurance coverage

Maintain appropriate professional liability, E&O, cyber liability, and crime coverage.

Pillar 7: Consumer complaints

Adopt written procedures for resolving consumer complaints.

For escrow managers, these pillars are not abstract compliance requirements. They show up in daily workflows, staff training, transaction handling, and audit preparation. Escrow managers are the operational owners responsible for implementation, consistency, and proof.

Understanding the pillars is only the starting point. The real challenge for escrow managers is not following these standards, but proving that they are followed consistently and completely.

Why audit-ready operations matter for escrow managers

The biggest risk for most escrow managers is being unable to prove compliance efficiently.

Manual processes, inconsistent documentation, and scattered records create exposure even when procedures are followed correctly. That gap becomes painful in four common situations:

- Lender questionnaires that demand documented procedures and verification logs

- SOC 2 reviews and compliance audits that require complete audit trails

- Cyber insurance renewals that need proof of security measures to avoid rate increases

- Multi-branch operations where inconsistency creates compliance gaps across locations

The shift required is fundamental. Moving from manual verification that relies on memory and notes to systematic approaches that create proof layers inside everyday workflows.

Audit-ready operations do not rely on people remembering to document. They build documentation into the process itself.

While all seven pillars matter, some create significantly more day-to-day exposure for escrow managers when audits and lender reviews occur.

ALTA best practices every escrow manager should prioritize

All seven ALTA pillars impact escrow operations, but some create more day-to-day exposure for escrow managers than others. What matters most is how each pillar shows up in real workflows and what auditors expect to see when they ask for proof.

You can reference the official ALTA Best Practices 4.2 Framework, effective August 19, 2025, for full requirements.

Pillar 1: Licensing

Title companies must establish and maintain all required licenses to conduct title insurance and settlement services.

For escrow managers, this means tracking business and individual licenses, meeting state requirements, maintaining Policy Forms Licensing compliance, and staying listed in the ALTA Registry.

Auditors look for proof that licensing is continuously monitored, including current certificates, renewal tracking with no lapses, and continuing education records. Helpful licensing resources include the NAIC State Licensing Map, ALTA Policy Forms Licensing, and the TIRS State Compliance Guide.

Pillar 2: Escrow trust accounting

Escrow trust accounting is one of the most heavily audited areas of ALTA compliance.

Requirements include properly identified trust accounts, no commingling of funds, and reconciliations that allow electronic verification.

Wire transfer procedures are central here. ALTA requires written protocols, annual testing, multi-factor authentication, and independent verification of wire instructions using secure software.

Manual callbacks and handwritten notes are common failure points. Tools like CertifID’s PayoffProtect automate verification and create timestamped audit trails. Auditors expect daily and monthly reconciliations, segregation of duties, management review, background checks, and wire fraud training.

Pillar 3: Protecting non-public information

This pillar requires a written information security plan and privacy plan to protect NPI under laws like the Gramm-Leach-Bliley Act.

Escrow managers are responsible for enforcing multi-factor authentication, password policies, access controls, and timely updates.

Proof includes access logs, encryption standards, annual security training records, incident response plans, and tested business continuity plans. Vendors with system access must align with these policies.

Additional guidance is available through the FTC Data Security Best Practices, FTC identity theft prevention guidance, and ALTA’s Business Continuity and Disaster Recovery guidance.

Pillar 4: Settlement processes (including wire fraud prevention)

Settlement processes include wire fraud prevention, the highest-risk area for escrow operations.

ALTA requires staff training, pricing controls, identity fraud prevention, and written wire transfer procedures tested annually. Response procedures should align with the ALTA Rapid Response Plan to ensure quick, coordinated action when fraud is suspected.

Auditors look for secure verification tools, multi-factor authentication, timestamped verification logs, and documented wire fraud response plans. Informal notes do not meet audit standards.

Pillar 5: Policy production

Title policies must be issued within required timeframes and reported accurately. Escrow managers must maintain written procedures, policy registers, timely reporting, and premium remittance records that demonstrate compliance.

Pillar 6: Insurance coverage

Companies must maintain appropriate E&O, cyber, and crime insurance. Proof includes current certificates, staff awareness of coverage limitations, and documented annual reviews with brokers.

Pillar 7: Consumer complaints

Written procedures must govern how complaints are received, escalated, and resolved. Auditors expect standardized forms tied to transactions, a designated point of contact, and complaint logs that track resolution.

This is where many escrow teams get stuck. They understand the requirements, but lack workflows that create audit-ready proof automatically.

How to operationalize ALTA best practices across your escrow team

The difference between compliance and audit readiness is the documentation created automatically through workflow.

Below is a simplified implementation framework.

For multi-branch operations, standardized workflows are critical. Every location must follow identical procedures. Central documentation repositories give auditors single-source access to records.

Technology that enforces protocols automatically removes reliance on memory and eliminates documentation gaps. To make this shift practical, escrow managers need a clear, time-bound plan.

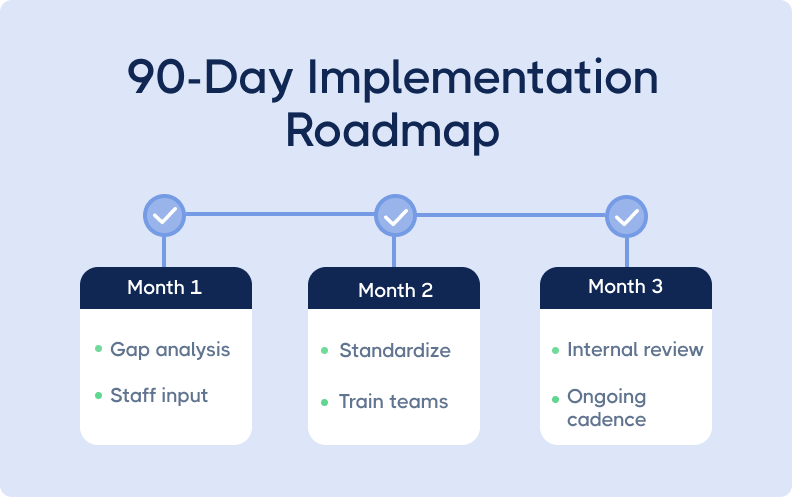

Your 90-day roadmap to ALTA compliance

Month 1: Assess

Audit current workflows against all seven ALTA pillars. Identify where documentation gaps create audit risk. Review past lender questionnaires and audit findings. Survey staff to understand where processes break under pressure.

Month 2: Implement

Develop standardized procedures, starting with wire fraud prevention. Train staff using ALTA resources and real case studies. Integrate verification tools where manual processes create gaps.

Month 3: Monitor

Run an internal review using an auditor’s lens. Organize documentation so records are easy to retrieve. Establish a quarterly review cadence to keep practices current.

Getting started with ALTA Best Practices

ALTA Best Practices are the operational framework for building an escrow operation that passes audits with confidence.

Escrow managers who treat compliance as a capability, not a task, reduce insurance costs, strengthen lender relationships, and scale more efficiently.

The work starts with understanding your current state across all seven pillars. Prioritize wire fraud prevention under Pillar 4, then build systems that create proof automatically so audit readiness becomes the default, not a scramble when questions arise.

For ongoing guidance, practical compliance protocols, and real-world fraud prevention insights, subscribe to our newsletter, The Wire. You’ll get educational resources designed to help escrow teams stay protected as threats and audit expectations continue to evolve.

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503