Secure online transactions: Why manual payoff checks are no longer enough

Manual payoff checks leave too much room for fraud. Learn how secure online tools protect every step of your transaction.

Share article:

Michelle Artreche

10 minutes

Digital Payments

Oct 7, 2025

Apr 22, 2026

73% of title companies closing over 250 deals monthly experienced increased cybercrime, compared to just 38% of smaller firms, according to ALTA's survey. As transaction volumes grow, so does your target on fraudsters' radar.

This threat coincides with real estate's shift toward online closings, making digital security more important than ever. Yet most title companies still rely on manual wire verification. It leads to wasted time, stressed staff, and gaps left that fraudsters exploit.

If you want to grow your title business, you can’t rely on legacy processes that are vulnerable. What you need instead are secure online transactions that eliminate fraud risks while helping you get more customers.

The real cost of "how we've always done it"

What feels like “business as usual” is often the single biggest drag on productivity and profit. Manual verification might seem harmless, but hidden costs add up fast.

The manual verification trap

Manual payoff verification eats hours every month through callbacks, database updates, and transcription errors. An escrow officer handling 50 closings can lose 16 hours a month to callbacks alone. Across five team members, that’s more than 80 hours monthly.

Add in hidden liabilities from inaccurate account details and human error, plus the inevitable burnout from juggling hundreds of closings with outdated tools. The operational toll becomes impossible to ignore.

There are proven ways to reduce the hours lost to callbacks and the risks of manual verification. The wire fraud prevention guide walks through practical steps and workflows to strengthen your process.

The fraud statistics that keep owners awake

Wire fraud continues its climb, with real estate losses hitting staggering numbers in 2024 and 2025.

According to the FBI’s Internet Crimes Complaint Center (IC3), total business email compromise losses surpassed $446 million in the real estate sector.

Median losses in payoff instruction fraud average $72,000 for buyers and $257,000 for title or law firms, with recovery rates under 30%. As insurers process more claims, premiums keep rising.

What are secure online title transactions?

Secure online title transactions rely on digital platforms that protect every aspect of property transfer, from initial identity verification through final fund disbursement.

These platforms integrate multiple layers of authentication, encryption, and fraud monitoring to create protection that traditional manual processes can't match.

The shift from manual workflows to digital platforms represents a change in how title companies approach security:

Common security risks in online title transactions

As title companies go digital, exposure to cyber threats rises. Business Email Compromise (BEC) scams alone cost 2,282 real estate victims nearly $446 million in 2022.

Not following ALTA best practices can add legal and financial risk. Using solid security measures and staying on top of compliance helps protect against these growing threats.

Why security is critical in online title transactions

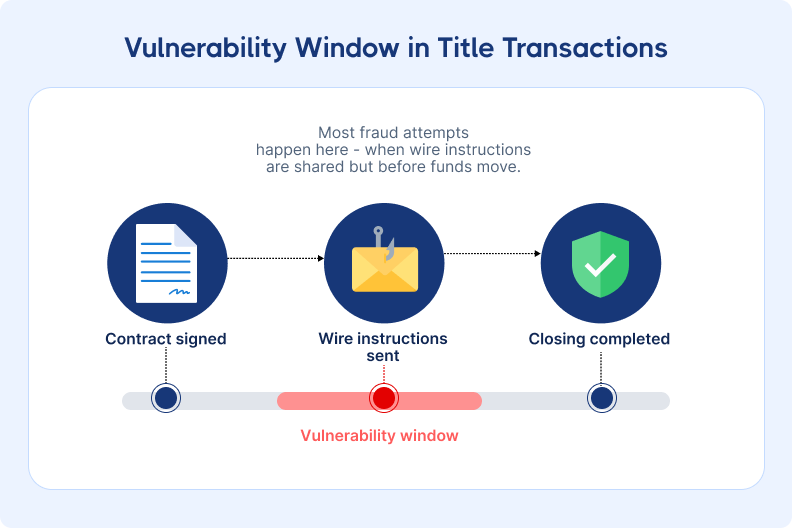

Most fraud happens in the 24-48 hours before closing when wire instructions are shared.

Digital transactions increase attack points. This creates new opportunities for fraudsters who now use AI-powered spoofing and social engineering to target agent, lender, and title company emails.

But the same digital shift also enables stronger protections when done right. Secure processes lower risk and legal liability.

So how do you build these stronger protections? Here are six best practices that leading title companies use to secure their transactions:

Best practice 1: Choose secure platforms designed for title transactions

Title companies with growth in mind are moving away from piecemeal security measures and building integrated security ecosystems. Instead of depending on a single solution, they are adopting a stack of specialized tools that work together to protect transactions from multiple angles.

The most resilient setups pair fraud-specific platforms with title production software integration, advanced email security, and real-time network monitoring.

The diagram below shows how the core components fit together to form a strong security foundation.

A fraud prevention platform like CertifID helps your escrow managers move money securely, authenticate identities, and streamline workflows, catching threats that might otherwise slip through. Integration with systems like SoftPro, Settlor, or AtClose allows these protections to operate without interrupting your daily workflows.

Email security with advanced threat protection blocks business email compromise attempts before they reach an inbox. Network monitoring adds another layer by detecting and responding to unusual activity.

Together, these tools create layered protection where each strengthens the others. Phasing in new technology, starting with fraud prevention, allows teams to adapt and confirm compatibility. Unified training reinforces a single, consistent security process, while centralized monitoring provides a clear view of threats and alerts.

Best practice 2: Use automated payoff and wire verification systems

Automating payoff and wire verification is one of the simplest ways to shut down a major risk in the escrow process. This is the window when large sums move based on documents that fraudsters target, and traditional “trust but verify” callbacks leave too much room for error.

Picture this: an escrow officer gets handwritten seller wire instructions for $400,000 in proceeds. Unsure of the account details, the seller copies them from an old checkbook.

Pressed for time, the officer makes a quick verification call and sends the wire. At every step (handwriting, transcription, phone verification), there’s a chance for mistakes or interception.

Here’s where the friction hides in a typical callback process:

.png)

Automated verification platforms cross-reference payoff details against millions of verified records, cutting the need for lengthy calls. Scanning tools pull data from the documents, so there’s no risk of manual entry mistakes. Most payoffs are confirmed in under a minute, and anything unusual is flagged for review.

With clear deadlines for changes, a full audit trail, and built-in insurance coverage, automation turns a high-risk process into one with documented proof at every step, keeping closings on track and fraud out of the picture.

Best practice 3: Implement identity verification protocols

Electronic signatures and remote online notarization have made closing a lot easier. But if you do not know for sure who is on the other end, you're taking a big risk. Identity verification stops that risk before it starts. Many fraudsters disappear the moment they are asked to show a valid ID.

The strongest systems check identity in more than one way. They scan a driver’s license, passport, or other government-issued ID and match it against trusted databases.

They confirm the person on camera is real and alive, not just a photo or video, with liveness detection. They add extra layers like personal history questions and database screening against fraud watchlists, making it even harder for someone to slip through unnoticed.

Some situations should always trigger these checks, like remote closings, vacant land sales, or transactions involving LLCs with unclear ownership.

By making identity verification a standard step for these scenarios, you cut off one of the easiest ways fraud can slip into a transaction.

Best practice 4: Deploy multi-layered cybersecurity measures

Even the best wire fraud prevention plan won’t work if your systems aren’t secure.

Think of cybersecurity as the locked front door that keeps bad actors out in the first place. The goal: close every potential entry point, protect sensitive information, and have a plan ready if someone slips through.

Start by locking down your network and systems. Firewalls, intrusion detection, and regular security audits can help spot weak points before criminals do.

Encrypt data, whether it is being sent or stored, and limit access so people only see what they need for their role. Back up your systems regularly and store some of those backups offline so they cannot be hit in an attack.

Protect every login with multi-factor authentication and strong passwords, and improve the process with single sign-on.

Automate updates, train staff to recognize scams, and have a clear incident response plan in place. Finally, don’t overlook your vendors; anyone handling your data should meet the same security standards you set for yourself.

When these layers work together, you build a much stronger shield against wire fraud. Use the quick checklist below to review and strengthen your defenses.

.png)

Best practice 5: Design secure verification workflows

Fraud prevention only works if people actually use it. If security slows people down, they’ll find workarounds. And these workarounds often carry vulnerabilities.

As one of the attorneys we interviewed noted, “Everything has to be verified by phone… we call up and we don’t use the phone number that is on the actual document.” This manual approach creates bottlenecks that modern workflows eliminate.

The sweet spot is security that feels almost invisible.

File-based processing organizes verifications by transaction instead of request, giving you one complete audit trail per closing.

Automated triggers prompt verification exactly when it’s needed, like when payoff statements arrive or seller proceeds are due. When something fails automated checks, clear exception protocols ensure manual review happens within 24–48 hours without throwing off the schedule.

Real-time tracking removes the “did I verify this?” uncertainty, while integration with title production software allows one-click verification and bulk processing. Priority queues keep urgent deals moving without cutting corners, and timestamped audit trails replace messy handwritten notes.

With the right workflows, security stops feeling like an obstacle and becomes part of how your team naturally works.

Best practice 6: Establish secure communication and client education protocols

Keeping your clients safe starts with how you communicate.

Our State of Wire Fraud 2025 report found that 52% of consumers are either not aware or only somewhat aware of wire fraud risks before closing. That’s a huge gap that you can close with secure channels and early education.

Use secure, branded portals so clients recognize your company throughout the process, which helps overcome resistance to unfamiliar systems.

For sensitive conversations, move beyond basic secure email to encrypted messaging platforms that include fraud monitoring. Always verify a client’s identity before sharing details, and keep complete records of every interaction so you have a clear audit trail.

And education is just as important as the tools. Only 49% of buyers and sellers hear about wire fraud from their real estate professionals, leaving many unprepared.

Take time to walk clients through common tactics, warning signs, and how wiring instructions are verified in your title company. When they understand the “why,” verification rates can soar up to 97%. Frame security as protection rather than a burden, and remember that consumers are willing to pay more for businesses that make safety a priority.

Why title companies are adapting these best practices

Title companies are making these best practices part of their process because they deliver relief now and position them to win later.

Escrow teams find that modern verification tools cut out the back-and-forth with buyers, reduce mistakes in payoff instructions, and let them spend more time on closings instead of callbacks.

For owners, the benefits stack up: less risk thanks to insurance-backed protection, the ability to grow without adding headcount, and a clear competitive edge when telling clients that their transactions are handled with top-tier security.

Secure online transactions: Manual payoff checks no longer cut it

Manual payoff checks just cannot keep up with how fast and clever fraudsters have become. The question is not if wire fraud will hit your business, but when. The good news is you can get ahead of it.

Start using secure online transaction tools that protect every step. Talk with vendors, see what fits your workflow, and make a plan to roll it out. The cost of sticking with manual methods is already higher than investing in security.

To see how to put these best practices into action, take a look at our resources on getting started with secure online title transactions.

FAQ

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

73% of title companies closing over 250 deals monthly experienced increased cybercrime, compared to just 38% of smaller firms, according to ALTA's survey. As transaction volumes grow, so does your target on fraudsters' radar.

This threat coincides with real estate's shift toward online closings, making digital security more important than ever. Yet most title companies still rely on manual wire verification. It leads to wasted time, stressed staff, and gaps left that fraudsters exploit.

If you want to grow your title business, you can’t rely on legacy processes that are vulnerable. What you need instead are secure online transactions that eliminate fraud risks while helping you get more customers.

The real cost of "how we've always done it"

What feels like “business as usual” is often the single biggest drag on productivity and profit. Manual verification might seem harmless, but hidden costs add up fast.

The manual verification trap

Manual payoff verification eats hours every month through callbacks, database updates, and transcription errors. An escrow officer handling 50 closings can lose 16 hours a month to callbacks alone. Across five team members, that’s more than 80 hours monthly.

Add in hidden liabilities from inaccurate account details and human error, plus the inevitable burnout from juggling hundreds of closings with outdated tools. The operational toll becomes impossible to ignore.

There are proven ways to reduce the hours lost to callbacks and the risks of manual verification. The wire fraud prevention guide walks through practical steps and workflows to strengthen your process.

The fraud statistics that keep owners awake

Wire fraud continues its climb, with real estate losses hitting staggering numbers in 2024 and 2025.

According to the FBI’s Internet Crimes Complaint Center (IC3), total business email compromise losses surpassed $446 million in the real estate sector.

Median losses in payoff instruction fraud average $72,000 for buyers and $257,000 for title or law firms, with recovery rates under 30%. As insurers process more claims, premiums keep rising.

What are secure online title transactions?

Secure online title transactions rely on digital platforms that protect every aspect of property transfer, from initial identity verification through final fund disbursement.

These platforms integrate multiple layers of authentication, encryption, and fraud monitoring to create protection that traditional manual processes can't match.

The shift from manual workflows to digital platforms represents a change in how title companies approach security:

Common security risks in online title transactions

As title companies go digital, exposure to cyber threats rises. Business Email Compromise (BEC) scams alone cost 2,282 real estate victims nearly $446 million in 2022.

Not following ALTA best practices can add legal and financial risk. Using solid security measures and staying on top of compliance helps protect against these growing threats.

Why security is critical in online title transactions

Most fraud happens in the 24-48 hours before closing when wire instructions are shared.

Digital transactions increase attack points. This creates new opportunities for fraudsters who now use AI-powered spoofing and social engineering to target agent, lender, and title company emails.

But the same digital shift also enables stronger protections when done right. Secure processes lower risk and legal liability.

So how do you build these stronger protections? Here are six best practices that leading title companies use to secure their transactions:

Best practice 1: Choose secure platforms designed for title transactions

Title companies with growth in mind are moving away from piecemeal security measures and building integrated security ecosystems. Instead of depending on a single solution, they are adopting a stack of specialized tools that work together to protect transactions from multiple angles.

The most resilient setups pair fraud-specific platforms with title production software integration, advanced email security, and real-time network monitoring.

The diagram below shows how the core components fit together to form a strong security foundation.

A fraud prevention platform like CertifID helps your escrow managers move money securely, authenticate identities, and streamline workflows, catching threats that might otherwise slip through. Integration with systems like SoftPro, Settlor, or AtClose allows these protections to operate without interrupting your daily workflows.

Email security with advanced threat protection blocks business email compromise attempts before they reach an inbox. Network monitoring adds another layer by detecting and responding to unusual activity.

Together, these tools create layered protection where each strengthens the others. Phasing in new technology, starting with fraud prevention, allows teams to adapt and confirm compatibility. Unified training reinforces a single, consistent security process, while centralized monitoring provides a clear view of threats and alerts.

Best practice 2: Use automated payoff and wire verification systems

Automating payoff and wire verification is one of the simplest ways to shut down a major risk in the escrow process. This is the window when large sums move based on documents that fraudsters target, and traditional “trust but verify” callbacks leave too much room for error.

Picture this: an escrow officer gets handwritten seller wire instructions for $400,000 in proceeds. Unsure of the account details, the seller copies them from an old checkbook.

Pressed for time, the officer makes a quick verification call and sends the wire. At every step (handwriting, transcription, phone verification), there’s a chance for mistakes or interception.

Here’s where the friction hides in a typical callback process:

Automated verification platforms cross-reference payoff details against millions of verified records, cutting the need for lengthy calls. Scanning tools pull data from the documents, so there’s no risk of manual entry mistakes. Most payoffs are confirmed in under a minute, and anything unusual is flagged for review.

With clear deadlines for changes, a full audit trail, and built-in insurance coverage, automation turns a high-risk process into one with documented proof at every step, keeping closings on track and fraud out of the picture.

Best practice 3: Implement identity verification protocols

Electronic signatures and remote online notarization have made closing a lot easier. But if you do not know for sure who is on the other end, you're taking a big risk. Identity verification stops that risk before it starts. Many fraudsters disappear the moment they are asked to show a valid ID.

The strongest systems check identity in more than one way. They scan a driver’s license, passport, or other government-issued ID and match it against trusted databases.

They confirm the person on camera is real and alive, not just a photo or video, with liveness detection. They add extra layers like personal history questions and database screening against fraud watchlists, making it even harder for someone to slip through unnoticed.

Some situations should always trigger these checks, like remote closings, vacant land sales, or transactions involving LLCs with unclear ownership.

By making identity verification a standard step for these scenarios, you cut off one of the easiest ways fraud can slip into a transaction.

Best practice 4: Deploy multi-layered cybersecurity measures

Even the best wire fraud prevention plan won’t work if your systems aren’t secure.

Think of cybersecurity as the locked front door that keeps bad actors out in the first place. The goal: close every potential entry point, protect sensitive information, and have a plan ready if someone slips through.

Start by locking down your network and systems. Firewalls, intrusion detection, and regular security audits can help spot weak points before criminals do.

Encrypt data, whether it is being sent or stored, and limit access so people only see what they need for their role. Back up your systems regularly and store some of those backups offline so they cannot be hit in an attack.

Protect every login with multi-factor authentication and strong passwords, and improve the process with single sign-on.

Automate updates, train staff to recognize scams, and have a clear incident response plan in place. Finally, don’t overlook your vendors; anyone handling your data should meet the same security standards you set for yourself.

When these layers work together, you build a much stronger shield against wire fraud. Use the quick checklist below to review and strengthen your defenses.

Best practice 5: Design secure verification workflows

Fraud prevention only works if people actually use it. If security slows people down, they’ll find workarounds. And these workarounds often carry vulnerabilities.

As one of the attorneys we interviewed noted, “Everything has to be verified by phone… we call up and we don’t use the phone number that is on the actual document.” This manual approach creates bottlenecks that modern workflows eliminate.

The sweet spot is security that feels almost invisible.

File-based processing organizes verifications by transaction instead of request, giving you one complete audit trail per closing.

Automated triggers prompt verification exactly when it’s needed, like when payoff statements arrive or seller proceeds are due. When something fails automated checks, clear exception protocols ensure manual review happens within 24–48 hours without throwing off the schedule.

Real-time tracking removes the “did I verify this?” uncertainty, while integration with title production software allows one-click verification and bulk processing. Priority queues keep urgent deals moving without cutting corners, and timestamped audit trails replace messy handwritten notes.

With the right workflows, security stops feeling like an obstacle and becomes part of how your team naturally works.

Best practice 6: Establish secure communication and client education protocols

Keeping your clients safe starts with how you communicate.

Our State of Wire Fraud 2025 report found that 52% of consumers are either not aware or only somewhat aware of wire fraud risks before closing. That’s a huge gap that you can close with secure channels and early education.

Use secure, branded portals so clients recognize your company throughout the process, which helps overcome resistance to unfamiliar systems.

For sensitive conversations, move beyond basic secure email to encrypted messaging platforms that include fraud monitoring. Always verify a client’s identity before sharing details, and keep complete records of every interaction so you have a clear audit trail.

And education is just as important as the tools. Only 49% of buyers and sellers hear about wire fraud from their real estate professionals, leaving many unprepared.

Take time to walk clients through common tactics, warning signs, and how wiring instructions are verified in your title company. When they understand the “why,” verification rates can soar up to 97%. Frame security as protection rather than a burden, and remember that consumers are willing to pay more for businesses that make safety a priority.

Why title companies are adapting these best practices

Title companies are making these best practices part of their process because they deliver relief now and position them to win later.

Escrow teams find that modern verification tools cut out the back-and-forth with buyers, reduce mistakes in payoff instructions, and let them spend more time on closings instead of callbacks.

For owners, the benefits stack up: less risk thanks to insurance-backed protection, the ability to grow without adding headcount, and a clear competitive edge when telling clients that their transactions are handled with top-tier security.

Secure online transactions: Manual payoff checks no longer cut it

Manual payoff checks just cannot keep up with how fast and clever fraudsters have become. The question is not if wire fraud will hit your business, but when. The good news is you can get ahead of it.

Start using secure online transaction tools that protect every step. Talk with vendors, see what fits your workflow, and make a plan to roll it out. The cost of sticking with manual methods is already higher than investing in security.

To see how to put these best practices into action, take a look at our resources on getting started with secure online title transactions.

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503