What are good funds? Guide for title companies and closing attorneys

Good funds are required to close. But 47 states define them differently, and the laws predate digital payments. This guide covers what qualifies and how to stay compliant.

Share article:

Jason Campbell

8 minutes

Good Funds

Feb 25, 2026

Apr 22, 2026

Title companies walk a tightrope between compliance requirements and buyer expectations for digital payments. Good funds laws—largely written in the 1970s-80s—create uncertainty about which modern payment methods meet state requirements.

Understanding compliant payment options is important for your competitive positioning. Title agencies and law firms offering convenient, compliant methods serve more buyers and close more deals.

This guide covers good funds fundamentals, state requirements, qualifying payment methods, and modernization strategies.

Understanding good funds: Definition and context

Good funds represent the foundation of secure real estate transactions, but their definition shifts between general banking and real estate-specific requirements. Here’s the breakdown.

Good funds in banking and finance

Good funds are verified liquid assets immediately available with zero reversal risk. Qualifying methods vary by market—some jurisdictions use the term “electronic transfers” which can create ambiguity about which payment types actually comply. Most commonly qualifying methods include:

- Wire transfers

- Cash

- Cashier's checks

- Certified checks

Personal checks, standard ACH, and credit cards do not qualify as good funds due to reversal risk. Personal checks take 3-5 business days to clear and can bounce. ACH reversals can occur up to 60 days post-posting under Federal Reserve ACH Operating Rules.

Good funds in real estate transactions

Good funds in real estate are instantly available, non-revocable payments required for closing, typically including wire transfers, cashier's checks, or certified checks.

State laws require these safeguards to protect against fraud and failed transactions that could derail closings. Texas Property Code §5.102 provides a concrete example of how states codify these requirements.

Here's where it gets complex: determining which payment rails actually qualify as good funds varies by state and often requires interpretation by underwriters or auditors. What's acceptable in California might not meet Florida's standards.

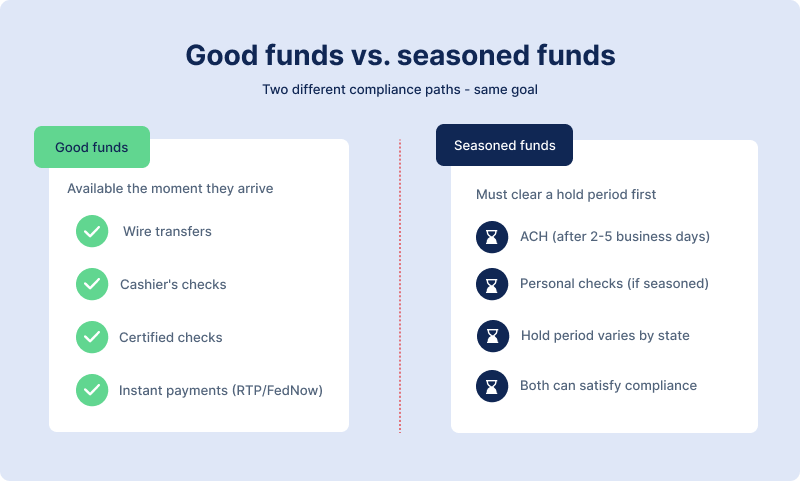

This is also where good funds and seasoned funds get confused. Good funds are available the moment they arrive—no waiting. Seasoned funds have cleared a mandatory hold period, typically 2-5 business days. Both can satisfy state requirements depending on the application: earnest money deposits, down payments, or closing disbursements. But the compliance path is different.

According to ALTA, 47 states have good funds laws with varying strictness. Some states enforce rigid requirements with clear penalties. Others provide general guidance, leaving room for interpretation. This variation creates challenges for multi-state operations in maintaining consistent compliance standards.

Types of compliant payment methods

Different payment methods offer varying levels of compliance, speed, and convenience for real estate transactions.

Traditional wire transfers

Wires are accepted in all 50 states as good funds without question. They provide immediate availability through the Federal Reserve Fedwire system with zero reversal risk once funds settle, typically within hours.

The drawbacks create friction:

- Expensive for buyers ($20-50 per transaction, according to NerdWallet)

- Inconvenient (requires physical bank visit)

- Prone to fraud if wire instructions are spoofed by cybercriminals

Wires remain the default in strict good funds states like Texas, Florida, and California, where alternatives face regulatory barriers.

According to Federal Reserve data, it processed an average of 869,187 transfers daily in 2025, with 1,148,267,267 in value of outgoing transfers.

Instant payment rails (RTP/FedNow)

Instant payment rails are real-time payment networks that enable immediate, irrevocable fund transfers between bank accounts. Unlike traditional payment methods that settle during business hours with delays, these networks operate continuously.

The Clearing House's RTP network launched in 2017, followed by the Federal Reserve's FedNow in 2023.

The key advantage: real-time settlement delivers funds in seconds, 24/7/365, with irrevocability, meeting the core good funds criterion.

The implementation reality requires coordination with your financial institution to understand specific requirements, costs and confirm their capabilities with these networks.

State good funds laws increasingly recognize instant payments as wire equivalents, though bank availability varies—not all institutions have adopted these capabilities yet.

Seasoned ACH payments

ACH can qualify as good funds with proper hold periods to mitigate reversal risk. The National Automated Clearing House Association (Nacha) processed 35.2 billion ACH transactions in 2025, valued at $93 trillion.

Typical seasoning requirements range from 2-5 business days, depending on state law and institutional policy. This waiting period exists because ACH returns can occur up to 60 days after posting for unauthorized transactions under Nacha Operating Rules.

Returns happen for a few reasons: insufficient funds, unauthorized transactions, or closed accounts. However, according to CertifID data, 95%+ of ACH returns occur within the first 2 business days of posting. This means the risk beyond this window is relatively small, though not zero.

State requirements vary significantly. Some states prohibit ACH entirely for earnest money deposits and cash to close, while others allow it with proper seasoning periods. Many title companies avoid ACH due to post-credit return risk and the reconciliation burden when returns do occur.

Modern digital payment platforms

Digital payment platforms bridge buyer convenience with title company and law firm compliance. Buyers initiate payments digitally through a simple, mobile-optimized experience, while title companies choose how they receive funds based on their state requirements and internal risk policies.

Three configuration options exist for earnest money deposits and cash to close:

- ACH: Digital initiation and delivery with a two-business-day hold period (buyer fee could be around $20)

- Instant (RTP/FedNow): Digital initiation, instant payment delivery via RTP/FedNow networks (widely recognized as meeting good funds standards, buyer fee of around $20)

- Wire: Digital initiation, wire delivery for strictest compliance requirements (buyer fee of around $28)

The guaranteed fund finality advantage: Leading platforms assume all ACH return risk once funds credit your escrow account. When funds arrive, they're final, and you can move forward with the transaction.

State-by-state good funds requirements

Good funds laws vary significantly across states. According to ALTA's survey and chart, 28 states and Washington, D.C. have good funds laws. RTP and FedNow are accepted or may be accepted in 28 states.

Even in strict states, individual companies may have different internal risk policies. Understand both state requirements and your company's risk parameters.

Why good funds matter for real estate transactions

Compliance matters from legal, operational, and competitive perspectives that impact your business.

Legal and compliance requirements

State laws mandate good funds to safeguard escrow accounts from fraud and failed transactions. The personal liability exposure is real: if you accept non-compliant funds that later fail, you're personally liable for covering the shortage.

The FBI's Internet Crime Complaint Center (IC3) reported $173.6 million in real estate fraud losses in 2024. Good funds laws exist precisely because of numbers like that—states built these rules to keep fraudulent or unstable funds out of escrow before they cause damage. But each state drew the line differently:

- Florida Rule 4-186.008: 24-hour hold common before disbursement

- Texas Insurance Code §2651.202: strict seasoning requirements

A single failed transaction can result in six-figure losses plus professional liability claims, regulatory penalties, and potential license suspension.

Buyers want a convenient digital payment experience

Buyers expect digital payment options matching their experience in other industries. Wire friction creates real barriers: $30-50 per transaction plus in-person bank visits during business hours—especially difficult for buyers juggling work schedules or purchasing remotely.

Real estate is modernizing with out-of-state purchases and online notarizations becoming standard, yet payment methods haven't kept pace.

The competitive reality: title companies offering convenient digital payment options attract more business, while wire-only operations face buyer complaints and lost deals.

Modern payment rails like instant payments (RTP/FedNow) and digital payment platforms now provide compliant alternatives to traditional wires. These methods align with good funds requirements while delivering the digital convenience buyers expect.

6 steps to verify good funds

Regardless of the payment method chosen, title companies can follow this six-step verification process to ensure good funds compliance.

Step 1: Receive deposit notification

Payment initiation begins when the buyer, agent, or lender submits funds.

Initial confirmation tasks include:

- Verify payment method being used

- Confirm expected delivery timeline

- Validate payment amount matches purchase agreement

Step 2: Verify payment rail and compliance

Confirm wire receipt or instant payment (RTP/FedNow) by accessing your bank portal or your secure payment verification software.

For ACH payments, verify the state-mandated seasoning period has been met (typically 2-5 business days). Cross-check against state-specific good funds statutes.

Never rely on email confirmations alone. Always verify through secure methods to prevent falling victim to spoofed wire confirmations.

Step 3: Validate fund availability

The validation checklist includes:

- Confirm funds have been posted to escrow account

- Verify payment metadata (buyer name, property address, file number)

- Match payment to correct transaction file in your system

Random wires arriving with minimal context create matching delays and force title agents to hunt for information, consuming 15-30 minutes per payment.

Step 4: Apply a hold period if required

State requirements vary—Texas requires stricter hold periods than California. Internal risk management policies may exceed state minimums as a business decision, not just regulatory compliance.

Federal Reserve banks are closed 11 days per year, and weekends add additional settlement delays. Check the Federal Reserve Bank Holiday Schedule when calculating hold periods.

Step 5: Document for compliance and audits

Documentation requirements include:

- Record payment rail used

- Document delivery date

- Note verification method employed

- File compliance documentation per state retention requirements

- Update transaction status in title production software

- Maintain complete audit trail for regulatory examinations

Step 6: Release funds

Final verification steps:

- Confirm all good funds requirements have been satisfied

- Authorize disbursement or application to closing costs

- Maintain records per state requirements (typically 5-7 years)

Common good funds: challenges and solutions

Title companies face practical problems when managing good funds compliance. Here's what actually happens and how to solve it.

Weekend and holiday payment delays

Federal Reserve banks are closed 11 days per year for federal holidays, and weekend closings extend settlement by 2-3 days. This creates unpredictable delays that can derail closing schedules. Check the Federal Reserve Holiday Schedule when planning closings.

Solutions include:

- Digital platforms with automatic holiday calculations show accurate delivery dates upfront

- Provide buyers with estimated delivery dates that account for non-business days, setting proper expectations

- Display holiday notifications proactively: "Memorial Day will delay processing by 1 business day"

- Plan closings with buffer time built in for payment settlement to avoid last-minute surprises

Payment tracking and file matching chaos

Random wires arriving with minimal context make it difficult to match payments to transaction files. Title agents waste 15-30 minutes per payment hunting for buyer information—this is pure operational inefficiency.

Solutions include:

- Require standardized payment metadata for all incoming payments: buyer name, property address, file number

- Digital platforms automatically include transaction details with every payment, solving the matching problem at the source

- Centralized payment tracking dashboards eliminate manual matching across multiple systems

- Real-time status visibility reduces "where's my payment?" support inquiries that consume staff time

Fraud prevention and verification

Fraud schemes are evolving—including spoofed wire confirmations and falsified cashier's checks.

Solutions include:

- Verify all wires through direct bank portal access or secure dedicated software—never trust email confirmations alone

- Verify identity of all parties involved in the transaction, no matter the size of it

- Implement identity verification (KYC) for all transaction parties

- Use account validation and balance checks before accepting any payment

- Deploy real-time fraud detection monitoring to catch suspicious patterns

ACH return risk and reconciliation burden

ACH payments can fail even after appearing in your escrow account. While 95%+ of returns occur within the first 2 business days, unauthorized returns can happen up to 60 days later, creating extended uncertainty. Review Nacha ACH Return Timeframes for specific windows.

Solutions include:

- Mandatory 2-3 business day hold periods before crediting escrow, waiting out the high-risk return window

- Modern platforms that assume post-credit ACH return risk, transferring the burden from title companies

- Automated return handling eliminates manual reconciliation when returns do occur

- For risk-averse operations, choose wire or instant payment configurations instead of ACH

- Conduct cost-benefit analysis: compare hold period delays against reconciliation burden

Good funds: Balancing compliance, security, and buyer experience

Good funds requirements protect title companies, buyers, and transaction integrity. The core principle remains constant: funds must be verified, immediately available, and irreversible before disbursement.

The challenge for modern title operations is meeting these requirements while delivering the digital convenience buyers expect. Traditional wire-only policies satisfy compliance but create competitive disadvantages and buyer friction.

The solution lies in understanding your state's specific requirements and selecting payment configurations that align with both compliance needs and operational goals.

Key considerations when selecting a payment solution:

- State compliance first: Verify if the solution meets your state's good funds requirements

- Risk tolerance: Determine how comfortable your company is with ACH return exposure

- Buyer experience: Consider how payment options impact buyers’ experience and your competitive positioning

- Operational efficiency: Evaluate time savings from automated tracking and metadata

- Fraud protection: Ensure built-in identity verification and account validation

- Transparency: Look for solutions with clear delivery timelines and status tracking

Review the ALTA Best Practices Framework for comprehensive guidance. Whether you operate in strict good funds states like Texas and Florida or more flexible jurisdictions, there are many compliant digital payment options..

By prioritizing fund verification, implementing proper hold periods, and choosing the right payment rails, title companies can modernize payment acceptance without compromising security or compliance.

Stay informed about wire fraud prevention and good funds compliance. Subscribe to our newsletter for monthly updates on fraud trends and compliance changes.

FAQ

How long must funds clear before closing?

Clearance time depends on payment method and state law. Wires and instant payments are immediate. ACH requires 2-5 business days. Check your state's specific statute—Texas and Florida have strict requirements.

Are personal checks considered good funds?

Rarely. Personal checks carry reversal risk and can take 3-5 days to clear. Most states prohibit them for earnest money. Illinois explicitly bans personal checks per 215 ILCS 155/26(c).

What are the penalties for accepting bad funds?

Title companies accepting non-compliant funds face personal liability for covering shortages if payments fail. This can result in six-figure losses, professional liability claims, regulatory penalties, and delayed closings.

Can title companies accept ACH for earnest money?

Depends on state law. Some states prohibit ACH entirely; others allow it with seasoning periods. Many title companies avoid ACH due to return risk. Modern solutions address this with hold periods and the assumption of post-credit risk.

Director of Payments Strategy

Jason Campbell serves as Director of Payments Strategy at CertifID. With over 20 years of experience spanning mortgage lending, escrow operations, and real estate technology, Jason has developed a comprehensive understanding of the complex financial workflows that underpin the real estate industry. At CertifID, Jason leverages this expertise to help shape payment strategy and advance the company's mission of protecting real estate transactions from wire fraud.

Title companies walk a tightrope between compliance requirements and buyer expectations for digital payments. Good funds laws—largely written in the 1970s-80s—create uncertainty about which modern payment methods meet state requirements.

Understanding compliant payment options is important for your competitive positioning. Title agencies and law firms offering convenient, compliant methods serve more buyers and close more deals.

This guide covers good funds fundamentals, state requirements, qualifying payment methods, and modernization strategies.

Understanding good funds: Definition and context

Good funds represent the foundation of secure real estate transactions, but their definition shifts between general banking and real estate-specific requirements. Here’s the breakdown.

Good funds in banking and finance

Good funds are verified liquid assets immediately available with zero reversal risk. Qualifying methods vary by market—some jurisdictions use the term “electronic transfers” which can create ambiguity about which payment types actually comply. Most commonly qualifying methods include:

- Wire transfers

- Cash

- Cashier's checks

- Certified checks

Personal checks, standard ACH, and credit cards do not qualify as good funds due to reversal risk. Personal checks take 3-5 business days to clear and can bounce. ACH reversals can occur up to 60 days post-posting under Federal Reserve ACH Operating Rules.

Good funds in real estate transactions

Good funds in real estate are instantly available, non-revocable payments required for closing, typically including wire transfers, cashier's checks, or certified checks.

State laws require these safeguards to protect against fraud and failed transactions that could derail closings. Texas Property Code §5.102 provides a concrete example of how states codify these requirements.

Here's where it gets complex: determining which payment rails actually qualify as good funds varies by state and often requires interpretation by underwriters or auditors. What's acceptable in California might not meet Florida's standards.

This is also where good funds and seasoned funds get confused. Good funds are available the moment they arrive—no waiting. Seasoned funds have cleared a mandatory hold period, typically 2-5 business days. Both can satisfy state requirements depending on the application: earnest money deposits, down payments, or closing disbursements. But the compliance path is different.

According to ALTA, 47 states have good funds laws with varying strictness. Some states enforce rigid requirements with clear penalties. Others provide general guidance, leaving room for interpretation. This variation creates challenges for multi-state operations in maintaining consistent compliance standards.

Types of compliant payment methods

Different payment methods offer varying levels of compliance, speed, and convenience for real estate transactions.

Traditional wire transfers

Wires are accepted in all 50 states as good funds without question. They provide immediate availability through the Federal Reserve Fedwire system with zero reversal risk once funds settle, typically within hours.

The drawbacks create friction:

- Expensive for buyers ($20-50 per transaction, according to NerdWallet)

- Inconvenient (requires physical bank visit)

- Prone to fraud if wire instructions are spoofed by cybercriminals

Wires remain the default in strict good funds states like Texas, Florida, and California, where alternatives face regulatory barriers.

According to Federal Reserve data, it processed an average of 869,187 transfers daily in 2025, with 1,148,267,267 in value of outgoing transfers.

Instant payment rails (RTP/FedNow)

Instant payment rails are real-time payment networks that enable immediate, irrevocable fund transfers between bank accounts. Unlike traditional payment methods that settle during business hours with delays, these networks operate continuously.

The Clearing House's RTP network launched in 2017, followed by the Federal Reserve's FedNow in 2023.

The key advantage: real-time settlement delivers funds in seconds, 24/7/365, with irrevocability, meeting the core good funds criterion.

The implementation reality requires coordination with your financial institution to understand specific requirements, costs and confirm their capabilities with these networks.

State good funds laws increasingly recognize instant payments as wire equivalents, though bank availability varies—not all institutions have adopted these capabilities yet.

Seasoned ACH payments

ACH can qualify as good funds with proper hold periods to mitigate reversal risk. The National Automated Clearing House Association (Nacha) processed 35.2 billion ACH transactions in 2025, valued at $93 trillion.

Typical seasoning requirements range from 2-5 business days, depending on state law and institutional policy. This waiting period exists because ACH returns can occur up to 60 days after posting for unauthorized transactions under Nacha Operating Rules.

Returns happen for a few reasons: insufficient funds, unauthorized transactions, or closed accounts. However, according to CertifID data, 95%+ of ACH returns occur within the first 2 business days of posting. This means the risk beyond this window is relatively small, though not zero.

State requirements vary significantly. Some states prohibit ACH entirely for earnest money deposits and cash to close, while others allow it with proper seasoning periods. Many title companies avoid ACH due to post-credit return risk and the reconciliation burden when returns do occur.

Modern digital payment platforms

Digital payment platforms bridge buyer convenience with title company and law firm compliance. Buyers initiate payments digitally through a simple, mobile-optimized experience, while title companies choose how they receive funds based on their state requirements and internal risk policies.

Three configuration options exist for earnest money deposits and cash to close:

- ACH: Digital initiation and delivery with a two-business-day hold period (buyer fee could be around $20)

- Instant (RTP/FedNow): Digital initiation, instant payment delivery via RTP/FedNow networks (widely recognized as meeting good funds standards, buyer fee of around $20)

- Wire: Digital initiation, wire delivery for strictest compliance requirements (buyer fee of around $28)

The guaranteed fund finality advantage: Leading platforms assume all ACH return risk once funds credit your escrow account. When funds arrive, they're final, and you can move forward with the transaction.

State-by-state good funds requirements

Good funds laws vary significantly across states. According to ALTA's survey and chart, 28 states and Washington, D.C. have good funds laws. RTP and FedNow are accepted or may be accepted in 28 states.

Even in strict states, individual companies may have different internal risk policies. Understand both state requirements and your company's risk parameters.

Why good funds matter for real estate transactions

Compliance matters from legal, operational, and competitive perspectives that impact your business.

Legal and compliance requirements

State laws mandate good funds to safeguard escrow accounts from fraud and failed transactions. The personal liability exposure is real: if you accept non-compliant funds that later fail, you're personally liable for covering the shortage.

The FBI's Internet Crime Complaint Center (IC3) reported $173.6 million in real estate fraud losses in 2024. Good funds laws exist precisely because of numbers like that—states built these rules to keep fraudulent or unstable funds out of escrow before they cause damage. But each state drew the line differently:

- Florida Rule 4-186.008: 24-hour hold common before disbursement

- Texas Insurance Code §2651.202: strict seasoning requirements

A single failed transaction can result in six-figure losses plus professional liability claims, regulatory penalties, and potential license suspension.

Buyers want a convenient digital payment experience

Buyers expect digital payment options matching their experience in other industries. Wire friction creates real barriers: $30-50 per transaction plus in-person bank visits during business hours—especially difficult for buyers juggling work schedules or purchasing remotely.

Real estate is modernizing with out-of-state purchases and online notarizations becoming standard, yet payment methods haven't kept pace.

The competitive reality: title companies offering convenient digital payment options attract more business, while wire-only operations face buyer complaints and lost deals.

Modern payment rails like instant payments (RTP/FedNow) and digital payment platforms now provide compliant alternatives to traditional wires. These methods align with good funds requirements while delivering the digital convenience buyers expect.

6 steps to verify good funds

Regardless of the payment method chosen, title companies can follow this six-step verification process to ensure good funds compliance.

Step 1: Receive deposit notification

Payment initiation begins when the buyer, agent, or lender submits funds.

Initial confirmation tasks include:

- Verify payment method being used

- Confirm expected delivery timeline

- Validate payment amount matches purchase agreement

Step 2: Verify payment rail and compliance

Confirm wire receipt or instant payment (RTP/FedNow) by accessing your bank portal or your secure payment verification software.

For ACH payments, verify the state-mandated seasoning period has been met (typically 2-5 business days). Cross-check against state-specific good funds statutes.

Never rely on email confirmations alone. Always verify through secure methods to prevent falling victim to spoofed wire confirmations.

Step 3: Validate fund availability

The validation checklist includes:

- Confirm funds have been posted to escrow account

- Verify payment metadata (buyer name, property address, file number)

- Match payment to correct transaction file in your system

Random wires arriving with minimal context create matching delays and force title agents to hunt for information, consuming 15-30 minutes per payment.

Step 4: Apply a hold period if required

State requirements vary—Texas requires stricter hold periods than California. Internal risk management policies may exceed state minimums as a business decision, not just regulatory compliance.

Federal Reserve banks are closed 11 days per year, and weekends add additional settlement delays. Check the Federal Reserve Bank Holiday Schedule when calculating hold periods.

Step 5: Document for compliance and audits

Documentation requirements include:

- Record payment rail used

- Document delivery date

- Note verification method employed

- File compliance documentation per state retention requirements

- Update transaction status in title production software

- Maintain complete audit trail for regulatory examinations

Step 6: Release funds

Final verification steps:

- Confirm all good funds requirements have been satisfied

- Authorize disbursement or application to closing costs

- Maintain records per state requirements (typically 5-7 years)

Common good funds: challenges and solutions

Title companies face practical problems when managing good funds compliance. Here's what actually happens and how to solve it.

Weekend and holiday payment delays

Federal Reserve banks are closed 11 days per year for federal holidays, and weekend closings extend settlement by 2-3 days. This creates unpredictable delays that can derail closing schedules. Check the Federal Reserve Holiday Schedule when planning closings.

Solutions include:

- Digital platforms with automatic holiday calculations show accurate delivery dates upfront

- Provide buyers with estimated delivery dates that account for non-business days, setting proper expectations

- Display holiday notifications proactively: "Memorial Day will delay processing by 1 business day"

- Plan closings with buffer time built in for payment settlement to avoid last-minute surprises

Payment tracking and file matching chaos

Random wires arriving with minimal context make it difficult to match payments to transaction files. Title agents waste 15-30 minutes per payment hunting for buyer information—this is pure operational inefficiency.

Solutions include:

- Require standardized payment metadata for all incoming payments: buyer name, property address, file number

- Digital platforms automatically include transaction details with every payment, solving the matching problem at the source

- Centralized payment tracking dashboards eliminate manual matching across multiple systems

- Real-time status visibility reduces "where's my payment?" support inquiries that consume staff time

Fraud prevention and verification

Fraud schemes are evolving—including spoofed wire confirmations and falsified cashier's checks.

Solutions include:

- Verify all wires through direct bank portal access or secure dedicated software—never trust email confirmations alone

- Verify identity of all parties involved in the transaction, no matter the size of it

- Implement identity verification (KYC) for all transaction parties

- Use account validation and balance checks before accepting any payment

- Deploy real-time fraud detection monitoring to catch suspicious patterns

ACH return risk and reconciliation burden

ACH payments can fail even after appearing in your escrow account. While 95%+ of returns occur within the first 2 business days, unauthorized returns can happen up to 60 days later, creating extended uncertainty. Review Nacha ACH Return Timeframes for specific windows.

Solutions include:

- Mandatory 2-3 business day hold periods before crediting escrow, waiting out the high-risk return window

- Modern platforms that assume post-credit ACH return risk, transferring the burden from title companies

- Automated return handling eliminates manual reconciliation when returns do occur

- For risk-averse operations, choose wire or instant payment configurations instead of ACH

- Conduct cost-benefit analysis: compare hold period delays against reconciliation burden

Good funds: Balancing compliance, security, and buyer experience

Good funds requirements protect title companies, buyers, and transaction integrity. The core principle remains constant: funds must be verified, immediately available, and irreversible before disbursement.

The challenge for modern title operations is meeting these requirements while delivering the digital convenience buyers expect. Traditional wire-only policies satisfy compliance but create competitive disadvantages and buyer friction.

The solution lies in understanding your state's specific requirements and selecting payment configurations that align with both compliance needs and operational goals.

Key considerations when selecting a payment solution:

- State compliance first: Verify if the solution meets your state's good funds requirements

- Risk tolerance: Determine how comfortable your company is with ACH return exposure

- Buyer experience: Consider how payment options impact buyers’ experience and your competitive positioning

- Operational efficiency: Evaluate time savings from automated tracking and metadata

- Fraud protection: Ensure built-in identity verification and account validation

- Transparency: Look for solutions with clear delivery timelines and status tracking

Review the ALTA Best Practices Framework for comprehensive guidance. Whether you operate in strict good funds states like Texas and Florida or more flexible jurisdictions, there are many compliant digital payment options..

By prioritizing fund verification, implementing proper hold periods, and choosing the right payment rails, title companies can modernize payment acceptance without compromising security or compliance.

Stay informed about wire fraud prevention and good funds compliance. Subscribe to our newsletter for monthly updates on fraud trends and compliance changes.

Director of Payments Strategy

Jason Campbell serves as Director of Payments Strategy at CertifID. With over 20 years of experience spanning mortgage lending, escrow operations, and real estate technology, Jason has developed a comprehensive understanding of the complex financial workflows that underpin the real estate industry. At CertifID, Jason leverages this expertise to help shape payment strategy and advance the company's mission of protecting real estate transactions from wire fraud.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503