Flexible earnest money deposits, built for how you operate

Three ways to receive EMDs. One secure, buyer-friendly experience—no compromises on compliance or risk.

Share article:

.png)

Cheryl Crouse

6 minutes

Digital Payments

Feb 13, 2026

Feb 24, 2026

For years, title companies have faced an impossible choice: accept wires to stay compliant, or accept ACH and deal with the chaos of returns and reconciliation.

CertifID's Digital Payments solution eliminates that tradeoff.

You can now choose how earnest money arrives—ACH, Instant Payments (RTP/FedNow), or Wire—based on your state requirements, risk tolerance, and operational needs. Every option includes the same core promise: guaranteed fund finality and built-in fraud protection.

Why flexibility matters for earnest money

No two title companies operate under the same conditions.

A Texas-based firm faces different good funds requirements than a company in Colorado. A team that’s been burned by ACH returns has a very different risk tolerance than one just starting to modernize payments. And buyers in highly competitive markets expect faster, more convenient options than those in areas where checks and wires still dominate.

One Colorado title company we spoke with accepts ACH for earnest money without issue. Their Texas counterpart operating 200 miles away legally cannot—state law requires immediate finality. A third company in Florida accepts ACH but manually holds funds for five days to avoid returns, creating constant "where's my money?" calls from impatient buyers.

Digital Payments lets all three operate the way their business requires.

With CertifID Digital Payments, you choose how earnest money is delivered to your escrow account based on your state requirements, internal policies, and risk posture. Buyers get the same modern, digital payment experience regardless of which configuration you select.

Three ways to accept earnest money

ACH

How it works: Buyers initiate payment via ACH debit from their bank account. After a two-business-day hold period, funds are delivered to your escrow account via ACH credit.

Who it's for: Title companies comfortable receiving ACH and want protection against post-credit returns without changing their existing payment rails.

Key benefits:

- Lowest buyer fee at $20 per transaction

- Familiar ACH delivery method

- Guaranteed fund finality—if a return happens after funds hit escrow, CertifID absorbs the loss and handles recovery

- No reconciliation or collections work for your team

- Refunds can be issued directly in the CertifID portal

Best fit if: You already accept ACH, your state allows ACH for earnest money, and you want buyer-friendly pricing without return risk.

Instant Payments (RTP/FedNow)

How it works: Buyers initiate payment via ACH debit. After the two-business-day hold period, funds are delivered to your escrow account via instant payment rails (RTP or FedNow).

Who it's for: Title companies whose banks support RTP or FedNow and want payment rails that align with strict good funds requirements without the friction of traditional wires.

Key benefits:

- Delivery via instant payment rails is commonly recognized under good funds laws

- Fast settlement once the hold period ends

- $20 buyer fee (same as ACH)

- Guaranteed funds with no clawbacks

- Modern payment infrastructure designed for speed and reliability

When to choose Instant: You need rails aligned with good funds standards but want faster delivery than traditional wires — without increasing buyer costs.

Wire

How it works: Buyers initiate payment digitally via ACH debit. After the two-business-day hold period, funds are delivered to your escrow account via wire transfer.

Who it's for: Title companies with the most conservative risk tolerance, those in strict good funds states, or operations with internal policies requiring wire-based payment delivery.

Why teams choose wire:

- Funds delivered via traditional wire rails

- Highest level of compliance confidence

- Guaranteed fund finality with no reversals

- Buyers never have to initiate a wire themselves

- Full fraud protection throughout the process

- No need to verify your bank supports instant payment rails

When to choose Wire: You operate in a state with strict good funds requirements, have internal policies against ACH risk, maintain ACH blocks on your escrow accounts, or simply prefer the assurance that comes with wire-based delivery. Additionally, the $28 buyer fee is still significantly less than traditional wire fees.

Good funds compliance without buyer friction

In states like Texas, California, and New York, good funds requirements often leave title companies with little flexibility. That usually means wires only — and a frustrating experience for buyers.

CertifID’s Instant and Wire configurations were built specifically to address this gap.

We recommend consulting your legal team on how these configurations align with your state's specific requirements. That said, Instant and Wire configurations deliver funds via payment rails—RTP, FedNow, and wire transfers—that are commonly recognized as meeting good funds operational standards in strict states like Texas, California, and New York.

What makes this approach different:

Payment rails that align with good funds thinking. RTP, FedNow, and wire transfers share the finality characteristics required for high-value transactions. These aren’t workarounds — they’re purpose-built rails.

Guaranteed finality, no exceptions. Once funds hit your escrow account, they’re final. If an ACH return occurs behind the scenes, CertifID handles it. No clawbacks, no reconciliation, no collections.

Compliance without sacrificing buyer experience. Buyers don’t need to visit a bank, decipher wire instructions, or pay $35–$50 in fees. They pay a clear $20–$28 fee, initiate payment digitally, and see exactly when funds will arrive.

The two-day hold

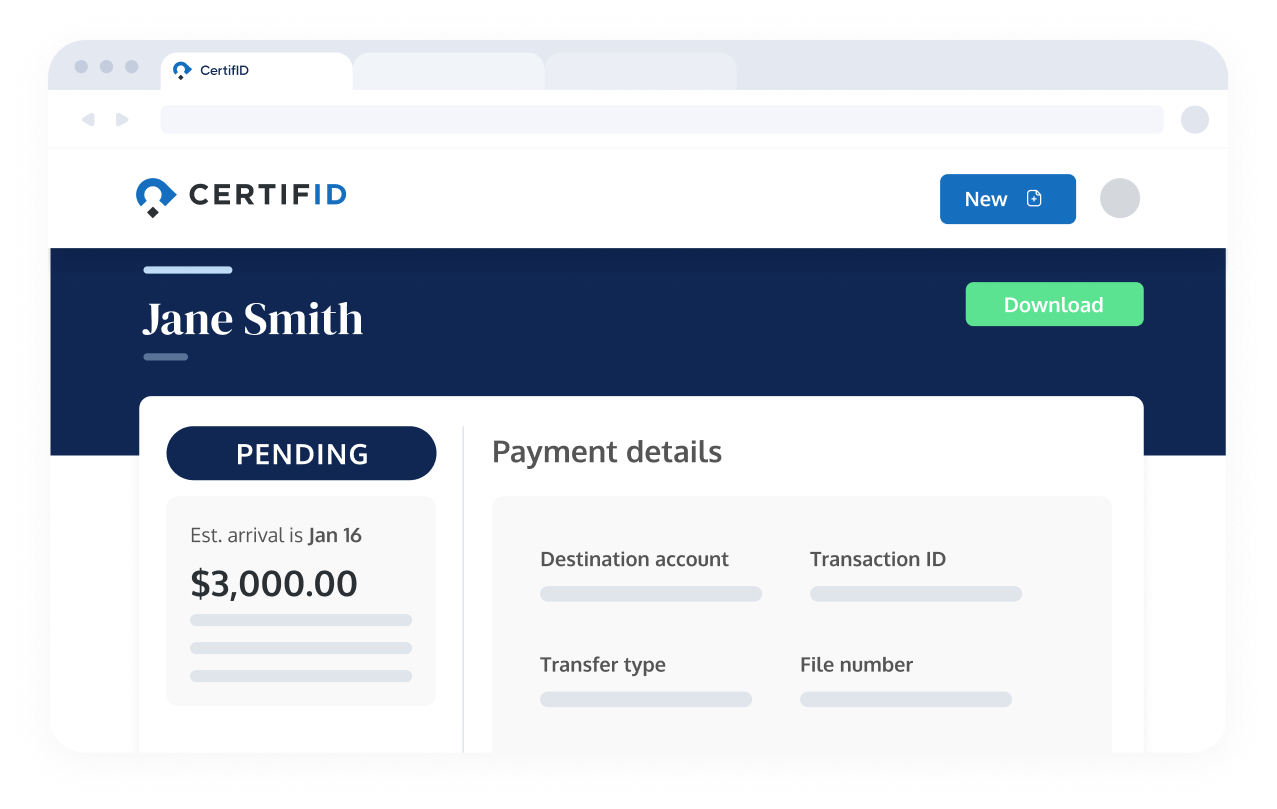

Why hold funds even for Wire and Instant configurations? Because all three options begin with ACH debit from the buyer's account. The hold period ensures the initial debit clears successfully before funds are converted to your chosen delivery rail (ACH, Instant, or Wire). This is what enables our fund finality guarantee across all configurations.

The system automatically accounts for weekends and bank holidays. Buyers see clear delivery estimates up front and receive notifications if holidays affect timing — eliminating “where’s my payment?” calls.

Beyond payment rails: what's included

While the configuration options are the headline feature, the solution as a whole is built around removing friction from the earnest money process:

Industry-leading fraud protection. Every transaction includes identity verification through KYC, account validation, balance checks, real-time fraud detection, and manual review when needed. All payments completed through the platform are fully insured.

Transparent timelines for everyone. Both buyers and title companies see estimated delivery dates before payment submission. No more ambiguity about when funds will arrive or whether a payment is "stuck" somewhere in the system.

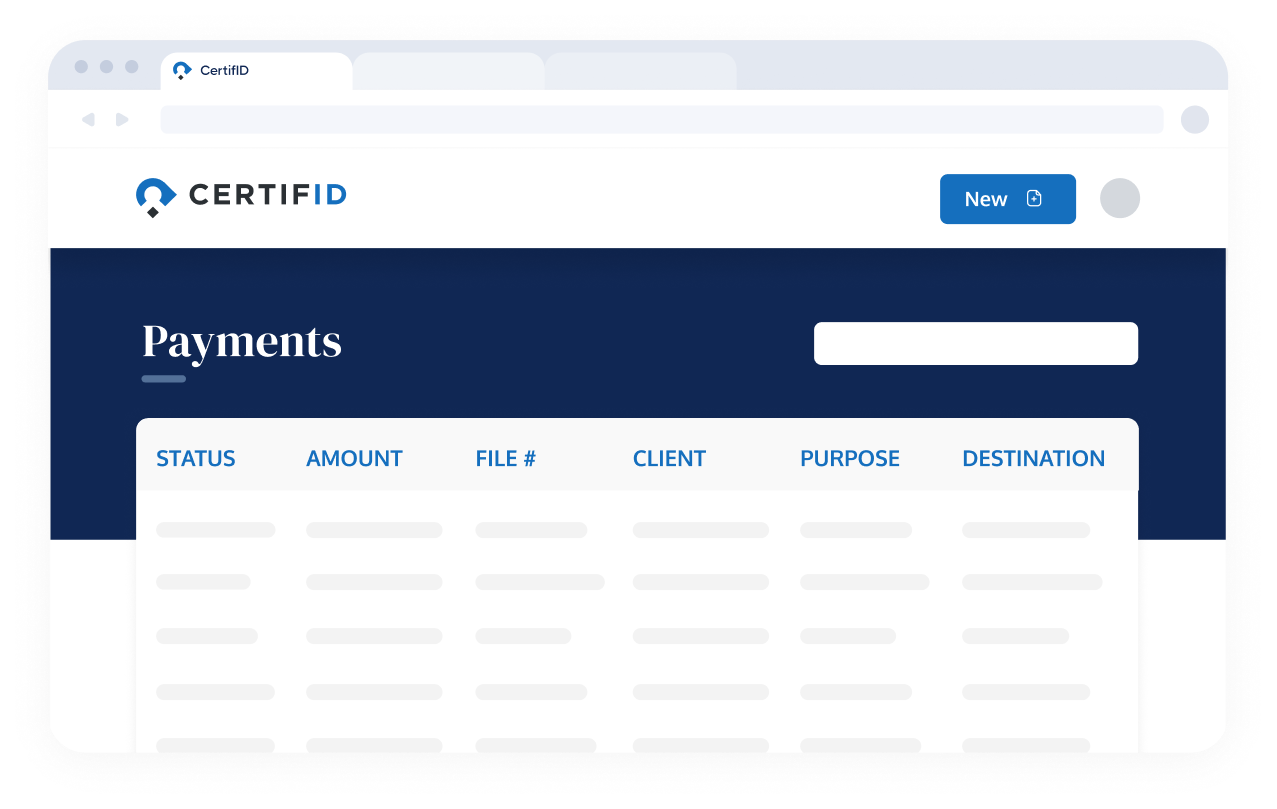

Complete payment metadata. Every payment includes buyer name, address, contact information, and payment details. Your team spends zero time hunting down who sent a payment or which file it belongs to.

24/7 buyer access. Homebuyers can initiate payments anytime, from any device, with no app download required. The mobile-optimized experience includes clear fee disclosure and step-by-step guidance.

Real-time tracking. The CertifID portal shows detailed activity timelines for each payment, from initiation through completion, so you always know exactly where funds are in the process.

How this changes your daily workflow

Consider how this changes your day-to-day operations:

No more check management: Eliminate the need to track physical checks, make bank runs, and wait for clearing periods. No more checks getting lost in the mail or sitting in someone's desk drawer.

No more wire coordination headaches: Stop fielding buyer complaints about bank wire fees, explaining complex wire instructions, or matching anonymous wire transfers to the correct files.

Clear compliance documentation: Every payment generates a complete audit trail showing identity verification, fraud checks, and fund finality guarantee—giving you defensible records if a transaction is ever questioned.

No more ACH return reconciliation: If you currently accept ACH, you know the pain of post-credit returns – updating accounting systems, tracking down buyers for repayment, dealing with closed or insufficient funds accounts. That entire burden disappears.

Predictable timelines for closing coordination: When you know exactly when funds will arrive, you can schedule closings with confidence. No more "waiting for the earnest money" delays.

Reduced support burden: Transparent delivery dates and real-time status tracking eliminate most "where's my payment?" inquiries from buyers and agents.

Built for what’s next

This isn't just about earnest money deposits. Digital Payments is built on infrastructure designed to scale across the transaction lifecycle. The same platform that supports EMDs today will power future payment types, including cash-to-close — giving you a single, secure way to move money from contract to closing.

Ready to get started?

For current CertifID customers: All three payment configurations are available now at no additional cost for per-file pricing customers. Talk to your Account Manager to choose which configuration aligns with your state requirements and risk policies. Most teams are live within 48 hours.

New to CertifID? Schedule a demo to see how Digital Payments works alongside wire verification, payoff validation, and identity checks in one connected platform.

The earnest money deposit process doesn't have to be a source of friction, risk, or buyer frustration. With Digital Payments, you can finally offer the flexibility buyers expect without compromising on compliance or taking on ACH risk.

FAQ

Senior Product Manager

Cheryl brings nearly a decade of product management experience in the real estate industry, making her mark at both scrappy startups and well-established companies. Driven by a deep customer focus and love for technology, she’s helped build innovative solutions that keep pace with evolving needs. At CertifID, Cheryl is helping drive the next phase of growth and push forward the mission to create a world without wire fraud.

For years, title companies have faced an impossible choice: accept wires to stay compliant, or accept ACH and deal with the chaos of returns and reconciliation.

CertifID's Digital Payments solution eliminates that tradeoff.

You can now choose how earnest money arrives—ACH, Instant Payments (RTP/FedNow), or Wire—based on your state requirements, risk tolerance, and operational needs. Every option includes the same core promise: guaranteed fund finality and built-in fraud protection.

Why flexibility matters for earnest money

No two title companies operate under the same conditions.

A Texas-based firm faces different good funds requirements than a company in Colorado. A team that’s been burned by ACH returns has a very different risk tolerance than one just starting to modernize payments. And buyers in highly competitive markets expect faster, more convenient options than those in areas where checks and wires still dominate.

One Colorado title company we spoke with accepts ACH for earnest money without issue. Their Texas counterpart operating 200 miles away legally cannot—state law requires immediate finality. A third company in Florida accepts ACH but manually holds funds for five days to avoid returns, creating constant "where's my money?" calls from impatient buyers.

Digital Payments lets all three operate the way their business requires.

With CertifID Digital Payments, you choose how earnest money is delivered to your escrow account based on your state requirements, internal policies, and risk posture. Buyers get the same modern, digital payment experience regardless of which configuration you select.

Three ways to accept earnest money

ACH

How it works: Buyers initiate payment via ACH debit from their bank account. After a two-business-day hold period, funds are delivered to your escrow account via ACH credit.

Who it's for: Title companies comfortable receiving ACH and want protection against post-credit returns without changing their existing payment rails.

Key benefits:

- Lowest buyer fee at $20 per transaction

- Familiar ACH delivery method

- Guaranteed fund finality—if a return happens after funds hit escrow, CertifID absorbs the loss and handles recovery

- No reconciliation or collections work for your team

- Refunds can be issued directly in the CertifID portal

Best fit if: You already accept ACH, your state allows ACH for earnest money, and you want buyer-friendly pricing without return risk.

Instant Payments (RTP/FedNow)

How it works: Buyers initiate payment via ACH debit. After the two-business-day hold period, funds are delivered to your escrow account via instant payment rails (RTP or FedNow).

Who it's for: Title companies whose banks support RTP or FedNow and want payment rails that align with strict good funds requirements without the friction of traditional wires.

Key benefits:

- Delivery via instant payment rails is commonly recognized under good funds laws

- Fast settlement once the hold period ends

- $20 buyer fee (same as ACH)

- Guaranteed funds with no clawbacks

- Modern payment infrastructure designed for speed and reliability

When to choose Instant: You need rails aligned with good funds standards but want faster delivery than traditional wires — without increasing buyer costs.

Wire

How it works: Buyers initiate payment digitally via ACH debit. After the two-business-day hold period, funds are delivered to your escrow account via wire transfer.

Who it's for: Title companies with the most conservative risk tolerance, those in strict good funds states, or operations with internal policies requiring wire-based payment delivery.

Why teams choose wire:

- Funds delivered via traditional wire rails

- Highest level of compliance confidence

- Guaranteed fund finality with no reversals

- Buyers never have to initiate a wire themselves

- Full fraud protection throughout the process

- No need to verify your bank supports instant payment rails

When to choose Wire: You operate in a state with strict good funds requirements, have internal policies against ACH risk, maintain ACH blocks on your escrow accounts, or simply prefer the assurance that comes with wire-based delivery. Additionally, the $28 buyer fee is still significantly less than traditional wire fees.

Good funds compliance without buyer friction

In states like Texas, California, and New York, good funds requirements often leave title companies with little flexibility. That usually means wires only — and a frustrating experience for buyers.

CertifID’s Instant and Wire configurations were built specifically to address this gap.

We recommend consulting your legal team on how these configurations align with your state's specific requirements. That said, Instant and Wire configurations deliver funds via payment rails—RTP, FedNow, and wire transfers—that are commonly recognized as meeting good funds operational standards in strict states like Texas, California, and New York.

What makes this approach different:

Payment rails that align with good funds thinking. RTP, FedNow, and wire transfers share the finality characteristics required for high-value transactions. These aren’t workarounds — they’re purpose-built rails.

Guaranteed finality, no exceptions. Once funds hit your escrow account, they’re final. If an ACH return occurs behind the scenes, CertifID handles it. No clawbacks, no reconciliation, no collections.

Compliance without sacrificing buyer experience. Buyers don’t need to visit a bank, decipher wire instructions, or pay $35–$50 in fees. They pay a clear $20–$28 fee, initiate payment digitally, and see exactly when funds will arrive.

The two-day hold

Why hold funds even for Wire and Instant configurations? Because all three options begin with ACH debit from the buyer's account. The hold period ensures the initial debit clears successfully before funds are converted to your chosen delivery rail (ACH, Instant, or Wire). This is what enables our fund finality guarantee across all configurations.

The system automatically accounts for weekends and bank holidays. Buyers see clear delivery estimates up front and receive notifications if holidays affect timing — eliminating “where’s my payment?” calls.

Beyond payment rails: what's included

While the configuration options are the headline feature, the solution as a whole is built around removing friction from the earnest money process:

Industry-leading fraud protection. Every transaction includes identity verification through KYC, account validation, balance checks, real-time fraud detection, and manual review when needed. All payments completed through the platform are fully insured.

Transparent timelines for everyone. Both buyers and title companies see estimated delivery dates before payment submission. No more ambiguity about when funds will arrive or whether a payment is "stuck" somewhere in the system.

Complete payment metadata. Every payment includes buyer name, address, contact information, and payment details. Your team spends zero time hunting down who sent a payment or which file it belongs to.

24/7 buyer access. Homebuyers can initiate payments anytime, from any device, with no app download required. The mobile-optimized experience includes clear fee disclosure and step-by-step guidance.

Real-time tracking. The CertifID portal shows detailed activity timelines for each payment, from initiation through completion, so you always know exactly where funds are in the process.

How this changes your daily workflow

Consider how this changes your day-to-day operations:

No more check management: Eliminate the need to track physical checks, make bank runs, and wait for clearing periods. No more checks getting lost in the mail or sitting in someone's desk drawer.

No more wire coordination headaches: Stop fielding buyer complaints about bank wire fees, explaining complex wire instructions, or matching anonymous wire transfers to the correct files.

Clear compliance documentation: Every payment generates a complete audit trail showing identity verification, fraud checks, and fund finality guarantee—giving you defensible records if a transaction is ever questioned.

No more ACH return reconciliation: If you currently accept ACH, you know the pain of post-credit returns – updating accounting systems, tracking down buyers for repayment, dealing with closed or insufficient funds accounts. That entire burden disappears.

Predictable timelines for closing coordination: When you know exactly when funds will arrive, you can schedule closings with confidence. No more "waiting for the earnest money" delays.

Reduced support burden: Transparent delivery dates and real-time status tracking eliminate most "where's my payment?" inquiries from buyers and agents.

Built for what’s next

This isn't just about earnest money deposits. Digital Payments is built on infrastructure designed to scale across the transaction lifecycle. The same platform that supports EMDs today will power future payment types, including cash-to-close — giving you a single, secure way to move money from contract to closing.

Ready to get started?

For current CertifID customers: All three payment configurations are available now at no additional cost for per-file pricing customers. Talk to your Account Manager to choose which configuration aligns with your state requirements and risk policies. Most teams are live within 48 hours.

New to CertifID? Schedule a demo to see how Digital Payments works alongside wire verification, payoff validation, and identity checks in one connected platform.

The earnest money deposit process doesn't have to be a source of friction, risk, or buyer frustration. With Digital Payments, you can finally offer the flexibility buyers expect without compromising on compliance or taking on ACH risk.

Senior Product Manager

Cheryl brings nearly a decade of product management experience in the real estate industry, making her mark at both scrappy startups and well-established companies. Driven by a deep customer focus and love for technology, she’s helped build innovative solutions that keep pace with evolving needs. At CertifID, Cheryl is helping drive the next phase of growth and push forward the mission to create a world without wire fraud.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503