Protecting real estate deals from growing check fraud

Why checks are still a top target for fraud and how to protect your transactions.

Share article:

Michelle Artreche

8 minutes

Fraud Prevention

Aug 12, 2025

Apr 22, 2026

Check fraud: What is it, how to spot and avoid losses?

When Tom Cronkright received a $180,000 certified check at Sun Title, everything looked legitimate. His business banker even confirmed: “No alerts, you’re good to go.” But three days after wiring the funds, the check bounced.

Check fraud doesn’t strike immediately. It lures you in, then hits after you’ve already acted, exploiting the gap between deposit and discovery. That delay makes it one of the most dangerous threats to real estate and small businesses today.

Here’s how to spot it, stop it, and avoid becoming the next victim.

What is check fraud and how does it work?

Check fraud is the unauthorized use of a check to obtain money or goods illegally. It can involve forgery, alterations, or complete counterfeiting.

Despite the rise of digital payments, checks remain a target because banks often make funds “available” before fully verifying them.

Provisional credit can appear within a day, while true verification takes several days, a gap fraudsters exploit.

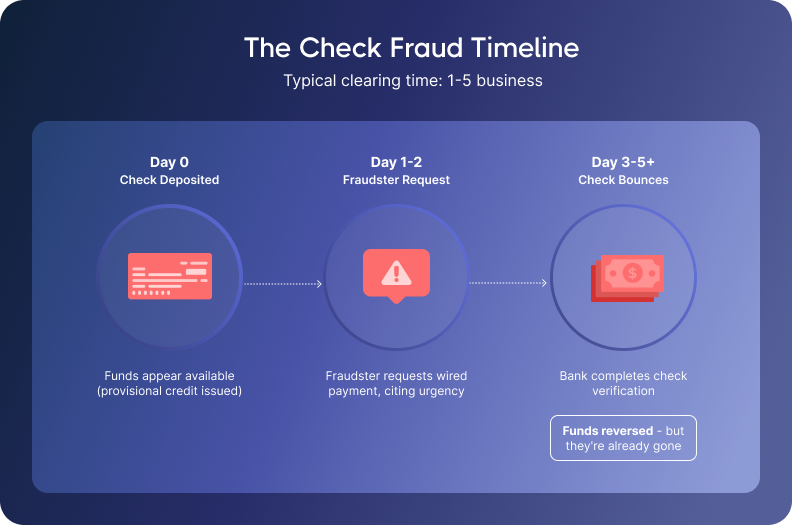

To understand why check fraud is so effective, it helps to see the timeline in action.

This built-in delay is the perfect setup for fraud: victims think they’re in the clear, only to be hit with a bounced check days later. Let’s break down how this type of fraud unfolds.

How check fraud works: The four-step process

1. Getting the check

Fraudsters start by getting their hands on real checks, usually stolen from residential mailboxes, business drop boxes, or purchased on the dark web.

2. Altering or counterfeiting

Checks are either chemically “washed” to erase and replace the payee and amount, or entirely counterfeited using high-resolution printers and design software.

3. Cashing or depositing

The altered or fake checks are deposited or cashed, often at ATMs or during busy banking hours.

4. Exploiting the delay

They count on the bank granting provisional credit before the check fully clears, allowing them to disappear before detection.

Why is check fraud escalating?

While the scam isn’t new, AI now helps replicate logos, fonts, and signatures with alarming accuracy.

As Jason Campbell, Sr. Account Manager at CertifID, said: "Checkwashing has been around for years... What has changed is the AI and technology available that makes it even easier."

Coupled with stolen checks for sale on the dark web, fraud is easier and more scalable. In 2024, 63% of organizations faced attempted or actual check fraud, making it the top fraud type.

5 types of check fraud

Fraudsters have developed tactics that exploit weaknesses in how checks are stored, processed, and verified. Here are five of the most common:

1. Counterfeit checks

Fraudsters create fake checks that mimic real ones using design software and standard printers. They copy details like the routing and account numbers from actual checks and print entirely new versions. These fakes can be hard to spot at first glance, especially if they include elements like watermarks or company logos.

2. Stolen checks

Checks are stolen from residential mailboxes, business drop boxes, or through insider access. Fraudsters may cash them as-is, forge signatures, or make minor edits. Some use string or glue traps to “fish” mail from USPS blue boxes.

3. Altered checks (Check washing)

This method uses chemicals like acetone or bleach to erase original ink from a real check. The fraudster then writes in a new payee and amount, keeping the authentic signature and account number to make it seem valid.

4. Forged checks

Forged checks use a real account holder’s details but fake the signature. Sometimes, they study past transactions to mimic handwriting or signature styles, tricking banks into approving fraudulent withdrawals.

5. Check kiting and paper hanging

Check kiting involves writing checks between multiple accounts without sufficient funds, relying on processing delays to cover the gap. Paper hanging is writing checks from closed or fake accounts, with no intention of repayment, just long enough to gain goods or services.

Title companies have some unique challenges that make them more appealing targets for sophisticated fraud schemes.

Why title companies face the perfect storm of check fraud risk

Title companies are uniquely exposed. They manage large sums of money, face strict deadlines, and rely on a mix of digital and manual processes. This creates the perfect environment for fraud to slip through unnoticed.

High-stakes transactions attract fraudsters

Real estate deals involve large sums. Every earnest money deposit or payoff check is a potential fraud opportunity.

The clearing time gap creates maximum vulnerability

Title companies often disburse funds before checks fully clear, unaware that the money isn’t really there.

As Tom Cronkright puts it: “If I take even a certified check today at closing and I’m wiring an hour after for the seller, am I really wiring off those funds? Well, I’m really not.”

In his case, the check was deposited in Michigan but had to clear through Idaho and Montana, adding days of delay.

Closing deadline pressure amplifies risk

Everyone wants to close deals quickly: buyers, sellers, agents, and title companies. The pressure is heightened by generational expectations: younger buyers prefer fast, digital services, while many sellers still rely on checks.

In the rush to close, red flags can be overlooked. In one case, a $10,000 earnest money check for a $30,000 lot was accepted without much scrutiny because closing was the next day.

Check fraud can have serious consequences, primarily determining who is responsible for the lost funds, which depends on when the fraud is noticed. By the time it is flagged, the money has usually moved, leaving the title company liable instead of the bank.

Who is liable for check fraud?

Check fraud often impacts those who discover it last, usually placing liability on businesses that acted in good faith, such as title companies.

Discovery timing determines liability

Banks usually require fraud to be reported within 24–48 hours of discovery, not from the check’s deposit. That’s a problem when title companies disburse funds based on checks that appear cleared. If the fraud isn’t caught right away, the money’s gone, and businesses must show they took “reasonable” steps to mitigate the risk.

Business exposure in real estate

Check fraud can derail closings and destroy trust. For closing attorneys, even one fraudulent check can lead to personal liability and malpractice claims, despite following procedures.

Insurance may not provide relief; many policies exclude coverage for check fraud or require verification steps that aren’t practical. Title companies also have a fiduciary obligation to verify funds, but often lack the necessary tools, creating a significant risk.

Bank liability limitations

Banks are protected under the Uniform Commercial Code (UCC) and aren’t held liable for properly negotiated checks, even if they're counterfeit.

This gives a false sense of security. Many hear, “There are no alerts, you’re good to go,” from their banks. But in reality, banks don’t have the tools to fully verify a check’s legitimacy.

Even if a check is clearly fake, if the bank followed standard procedures, your options for recourse are limited.

Check scam warning signs that require immediate verification

Check fraud scams tend to follow recognizable patterns. It’s all about knowing what to look for and taking red flags seriously, even under time pressure.

Amount and timing red flags

Unusually large earnest money checks can be suspicious, especially if they don’t match the property value.

Another red flag is offering round numbers, such as $5,000 or $10,000, instead of precise amounts like $1,247. Fraudsters pair these red flags with tight deadlines like “must close by Friday,” hoping to pressure you into disbursing funds quickly.

Geographic and behavioral inconsistencies

Small details can expose scams. An out-of-state buyer presenting a check from a local bank should raise questions. Vague backstories or sudden changes, like payment methods after check delivery, are tactics to blur the paper trail.

Pressure tactics

Fraudsters create urgency to lower your guard. They may cite last-minute issues, push emotional excuses, or ask you to bend the rules “just this once.” It’s important to recognize that these are tests of your boundaries rather than just standard procedures.

Recognizing these tactics matters, but true protection comes from systems that remove the need for split-second judgment calls under pressure.

How to prevent check fraud: 5 best practices for businesses

The most effective way to prevent check fraud is to accept a simple truth: visual inspection and early bank assurances aren’t enough. You need verification protocols that reflect how checks actually clear.

1. Verification protocols that match clearing reality

Don’t mistake “cleared” for “verified.”

Banks often show funds as available before confirming a check is legitimate, a gap fraudsters rely on. For large deposits, call the issuing bank directly and ask: “Did you create this check?” and “Is this check yours?” If they can’t confirm, don’t proceed.

2. Banking technology and controls

Many banks offer low-cost tools like positive pay, which alerts you when check details don’t match your submissions. Daily reconciliation can help catch anomalies early. Ensure your setup is strong by understanding your bank’s verification limits and adding your own checks.

3. Policy controls that eliminate timing vulnerabilities

Set check deposit rules. Wait for full clearing confirmation before wiring funds. Maintain custody protocols; consider checks final once released. For larger transactions, require dual authorization and train staff to recognize red flags, even when timelines are tight.

4. Physical security measures

Limit access to blank checks and store them securely. Use tamper-evident checks to make alterations easier to spot. And ensure secure handling of any mail that includes checks, both incoming and outgoing.

5. Technology solutions that eliminate the problem

Digital payments offer instant confirmation and traceability, eliminating gaps left by checks. They confirm transactions in real time and include a detailed audit trail.

Today, customers expect to pay electronically. Tom says, “85% of our first-time home buyers prefer/demand an electronic payment option.” Beyond convenience, the ROI is clear: investing in technology that prevents fraud is far less costly than recovering from it.

But if fraud happens, what matters is how you respond.

What to do when check fraud occurs

When check fraud hits, every minute counts. Acting quickly can help you recover your money before it's too late.

Immediate response protocol

Speed is your best defense against fraud. Contact your bank immediately to request a hold or reversal of the transaction. The sooner they’re aware, the better your chances.

Document all details: when the check was deposited, when you noticed the issue, and any related communications. These records are crucial for proving liability.

Finally, report the incident to law enforcement while the transaction trail is still fresh. Once funds are withdrawn or sent elsewhere, it's hard to recover them. That's why taking quick action is so important.

Check fraud: Protect every payment before it’s too late

What makes check fraud so dangerous is the lag. You deposit the check, release the funds, and only find out days later that it was fake. That timing gap cost Tom $180,000. It wasn’t carelessness; it’s a system that favors fraudsters.

In real estate, where every moment counts and the stakes are high, finding out about these issues late can really hurt. It’s important to think about whether your current processes take these check-clearing delays into account.

The good news is that the industry is shifting toward instant, verified payments. Are you ready to adapt, or will you find yourself playing catch-up?

FAQ

How long does it really take for a check to clear?

Normally, it can take around 1 to 3 business days, but keep in mind that delays might happen based on where you are and how banks process things.

Can I act on funds before they fully clear?

Legally, yes, but it’s risky. Fraudsters count on this window to exploit your trust.

When does liability protection begin?

When you report the fraud. The sooner you act, the better.

What’s the main difference between check and wire fraud?

Wire fraud is instantly detectable. Check fraud hides in the lag, often surfacing only after damage is done.

Are certified checks safer?

Not always. As Tom learned, a claim of “certified check” means nothing without verification.

What should I do if I suspect check fraud?

Don’t wait! Contact your bank and file a police report right away. Every hour counts.

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

Check fraud: What is it, how to spot and avoid losses?

When Tom Cronkright received a $180,000 certified check at Sun Title, everything looked legitimate. His business banker even confirmed: “No alerts, you’re good to go.” But three days after wiring the funds, the check bounced.

Check fraud doesn’t strike immediately. It lures you in, then hits after you’ve already acted, exploiting the gap between deposit and discovery. That delay makes it one of the most dangerous threats to real estate and small businesses today.

Here’s how to spot it, stop it, and avoid becoming the next victim.

What is check fraud and how does it work?

Check fraud is the unauthorized use of a check to obtain money or goods illegally. It can involve forgery, alterations, or complete counterfeiting.

Despite the rise of digital payments, checks remain a target because banks often make funds “available” before fully verifying them.

Provisional credit can appear within a day, while true verification takes several days, a gap fraudsters exploit.

To understand why check fraud is so effective, it helps to see the timeline in action.

This built-in delay is the perfect setup for fraud: victims think they’re in the clear, only to be hit with a bounced check days later. Let’s break down how this type of fraud unfolds.

How check fraud works: The four-step process

1. Getting the check

Fraudsters start by getting their hands on real checks, usually stolen from residential mailboxes, business drop boxes, or purchased on the dark web.

2. Altering or counterfeiting

Checks are either chemically “washed” to erase and replace the payee and amount, or entirely counterfeited using high-resolution printers and design software.

3. Cashing or depositing

The altered or fake checks are deposited or cashed, often at ATMs or during busy banking hours.

4. Exploiting the delay

They count on the bank granting provisional credit before the check fully clears, allowing them to disappear before detection.

Why is check fraud escalating?

While the scam isn’t new, AI now helps replicate logos, fonts, and signatures with alarming accuracy.

As Jason Campbell, Sr. Account Manager at CertifID, said: "Checkwashing has been around for years... What has changed is the AI and technology available that makes it even easier."

Coupled with stolen checks for sale on the dark web, fraud is easier and more scalable. In 2024, 63% of organizations faced attempted or actual check fraud, making it the top fraud type.

5 types of check fraud

Fraudsters have developed tactics that exploit weaknesses in how checks are stored, processed, and verified. Here are five of the most common:

1. Counterfeit checks

Fraudsters create fake checks that mimic real ones using design software and standard printers. They copy details like the routing and account numbers from actual checks and print entirely new versions. These fakes can be hard to spot at first glance, especially if they include elements like watermarks or company logos.

2. Stolen checks

Checks are stolen from residential mailboxes, business drop boxes, or through insider access. Fraudsters may cash them as-is, forge signatures, or make minor edits. Some use string or glue traps to “fish” mail from USPS blue boxes.

3. Altered checks (Check washing)

This method uses chemicals like acetone or bleach to erase original ink from a real check. The fraudster then writes in a new payee and amount, keeping the authentic signature and account number to make it seem valid.

4. Forged checks

Forged checks use a real account holder’s details but fake the signature. Sometimes, they study past transactions to mimic handwriting or signature styles, tricking banks into approving fraudulent withdrawals.

5. Check kiting and paper hanging

Check kiting involves writing checks between multiple accounts without sufficient funds, relying on processing delays to cover the gap. Paper hanging is writing checks from closed or fake accounts, with no intention of repayment, just long enough to gain goods or services.

Title companies have some unique challenges that make them more appealing targets for sophisticated fraud schemes.

Why title companies face the perfect storm of check fraud risk

Title companies are uniquely exposed. They manage large sums of money, face strict deadlines, and rely on a mix of digital and manual processes. This creates the perfect environment for fraud to slip through unnoticed.

High-stakes transactions attract fraudsters

Real estate deals involve large sums. Every earnest money deposit or payoff check is a potential fraud opportunity.

The clearing time gap creates maximum vulnerability

Title companies often disburse funds before checks fully clear, unaware that the money isn’t really there.

As Tom Cronkright puts it: “If I take even a certified check today at closing and I’m wiring an hour after for the seller, am I really wiring off those funds? Well, I’m really not.”

In his case, the check was deposited in Michigan but had to clear through Idaho and Montana, adding days of delay.

Closing deadline pressure amplifies risk

Everyone wants to close deals quickly: buyers, sellers, agents, and title companies. The pressure is heightened by generational expectations: younger buyers prefer fast, digital services, while many sellers still rely on checks.

In the rush to close, red flags can be overlooked. In one case, a $10,000 earnest money check for a $30,000 lot was accepted without much scrutiny because closing was the next day.

Check fraud can have serious consequences, primarily determining who is responsible for the lost funds, which depends on when the fraud is noticed. By the time it is flagged, the money has usually moved, leaving the title company liable instead of the bank.

Who is liable for check fraud?

Check fraud often impacts those who discover it last, usually placing liability on businesses that acted in good faith, such as title companies.

Discovery timing determines liability

Banks usually require fraud to be reported within 24–48 hours of discovery, not from the check’s deposit. That’s a problem when title companies disburse funds based on checks that appear cleared. If the fraud isn’t caught right away, the money’s gone, and businesses must show they took “reasonable” steps to mitigate the risk.

Business exposure in real estate

Check fraud can derail closings and destroy trust. For closing attorneys, even one fraudulent check can lead to personal liability and malpractice claims, despite following procedures.

Insurance may not provide relief; many policies exclude coverage for check fraud or require verification steps that aren’t practical. Title companies also have a fiduciary obligation to verify funds, but often lack the necessary tools, creating a significant risk.

Bank liability limitations

Banks are protected under the Uniform Commercial Code (UCC) and aren’t held liable for properly negotiated checks, even if they're counterfeit.

This gives a false sense of security. Many hear, “There are no alerts, you’re good to go,” from their banks. But in reality, banks don’t have the tools to fully verify a check’s legitimacy.

Even if a check is clearly fake, if the bank followed standard procedures, your options for recourse are limited.

Check scam warning signs that require immediate verification

Check fraud scams tend to follow recognizable patterns. It’s all about knowing what to look for and taking red flags seriously, even under time pressure.

Amount and timing red flags

Unusually large earnest money checks can be suspicious, especially if they don’t match the property value.

Another red flag is offering round numbers, such as $5,000 or $10,000, instead of precise amounts like $1,247. Fraudsters pair these red flags with tight deadlines like “must close by Friday,” hoping to pressure you into disbursing funds quickly.

Geographic and behavioral inconsistencies

Small details can expose scams. An out-of-state buyer presenting a check from a local bank should raise questions. Vague backstories or sudden changes, like payment methods after check delivery, are tactics to blur the paper trail.

Pressure tactics

Fraudsters create urgency to lower your guard. They may cite last-minute issues, push emotional excuses, or ask you to bend the rules “just this once.” It’s important to recognize that these are tests of your boundaries rather than just standard procedures.

Recognizing these tactics matters, but true protection comes from systems that remove the need for split-second judgment calls under pressure.

How to prevent check fraud: 5 best practices for businesses

The most effective way to prevent check fraud is to accept a simple truth: visual inspection and early bank assurances aren’t enough. You need verification protocols that reflect how checks actually clear.

1. Verification protocols that match clearing reality

Don’t mistake “cleared” for “verified.”

Banks often show funds as available before confirming a check is legitimate, a gap fraudsters rely on. For large deposits, call the issuing bank directly and ask: “Did you create this check?” and “Is this check yours?” If they can’t confirm, don’t proceed.

2. Banking technology and controls

Many banks offer low-cost tools like positive pay, which alerts you when check details don’t match your submissions. Daily reconciliation can help catch anomalies early. Ensure your setup is strong by understanding your bank’s verification limits and adding your own checks.

3. Policy controls that eliminate timing vulnerabilities

Set check deposit rules. Wait for full clearing confirmation before wiring funds. Maintain custody protocols; consider checks final once released. For larger transactions, require dual authorization and train staff to recognize red flags, even when timelines are tight.

4. Physical security measures

Limit access to blank checks and store them securely. Use tamper-evident checks to make alterations easier to spot. And ensure secure handling of any mail that includes checks, both incoming and outgoing.

5. Technology solutions that eliminate the problem

Digital payments offer instant confirmation and traceability, eliminating gaps left by checks. They confirm transactions in real time and include a detailed audit trail.

Today, customers expect to pay electronically. Tom says, “85% of our first-time home buyers prefer/demand an electronic payment option.” Beyond convenience, the ROI is clear: investing in technology that prevents fraud is far less costly than recovering from it.

But if fraud happens, what matters is how you respond.

What to do when check fraud occurs

When check fraud hits, every minute counts. Acting quickly can help you recover your money before it's too late.

Immediate response protocol

Speed is your best defense against fraud. Contact your bank immediately to request a hold or reversal of the transaction. The sooner they’re aware, the better your chances.

Document all details: when the check was deposited, when you noticed the issue, and any related communications. These records are crucial for proving liability.

Finally, report the incident to law enforcement while the transaction trail is still fresh. Once funds are withdrawn or sent elsewhere, it's hard to recover them. That's why taking quick action is so important.

Check fraud: Protect every payment before it’s too late

What makes check fraud so dangerous is the lag. You deposit the check, release the funds, and only find out days later that it was fake. That timing gap cost Tom $180,000. It wasn’t carelessness; it’s a system that favors fraudsters.

In real estate, where every moment counts and the stakes are high, finding out about these issues late can really hurt. It’s important to think about whether your current processes take these check-clearing delays into account.

The good news is that the industry is shifting toward instant, verified payments. Are you ready to adapt, or will you find yourself playing catch-up?

Content Marketer

Michelle has spent her career in B2B SaaS startups leading content marketing, strategy, and social media efforts that help teams grow and audiences stay informed. At CertifID, she applies that expertise to help title and real estate professionals understand fraud risks and stay ahead of emerging threats.

Sign up for The Wire to join the conversation.

.png)

Austin

3601 South Congress Ave.

Ste D200, Austin, Texas 78704

Grand Rapids

124 Fulton Street E

Grand Rapids, MI 49503